Ever feel like the markets are playing a game of financial limbo right before the Fed drops its latest rate decision? Tuesday’s trading session sure felt like that—a nervous shuffle, a cautious toe-dip in the water as investors held their breath for Wednesday’s big reveal. Stocks managed a timid climb on whispers of easing, yet the dollar wobbled like a tightrope walker, and Bitcoin staged a dramatic comeback from early losses. With whispers of hawkish cuts and central banks around the globe sending mixed signals, it’s a real cliffhanger out there. Wondering what nuggets you might’ve missed while dodging all the market noise? Dive in and get the full scoop on global forex shifts, job stats, and the ever-enticing tug-of-war between risk and refuge. Ready to unpack the full story? LEARN MORE.

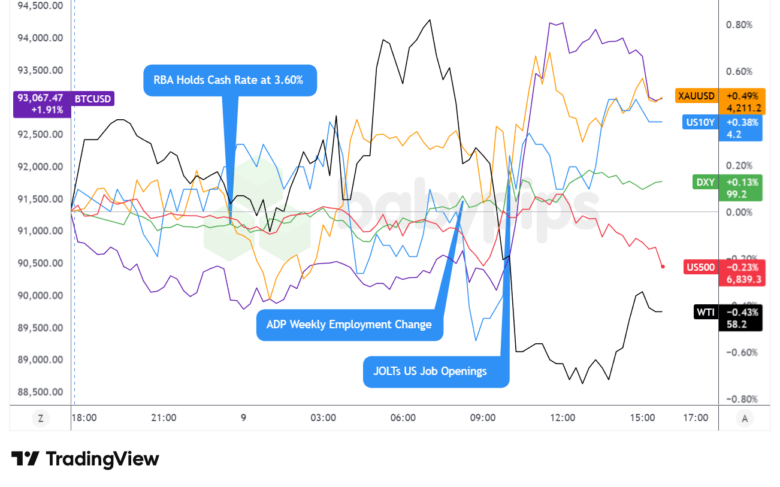

Reserve Bank of Australia holds cash rate at 3.60% as expected; Governor Bullock says board discussed circumstances requiring tightening, singles out February meeting for careful inflation watch

Australian November NAB business conditions +7 vs +9 priorU.K. BRC November retail sales +1.2% y/y vs +1.5% prior

Bank of Japan Governor Ueda says recent long-term rate rises have been “somewhat rapid,” signals BOJ could increase bond buying if neededGermany October trade balance €16.9B vs €15.6B expected

Trump tells Politico he may consider changes to tariffs to lower prices; calls willingness to lower rates a “litmus test” for Fed chair choice

ADP weekly employment data suggests private companies added modest 4,750 jobs per week through November 22

U.S. JOLTS Job Openings for October 2025: 7.67M (7.12M forecast; 7.74M previous) – highest since May but data delayed by government shutdown

Kevin Hassett says there’s “plenty of room” to cut rates substantially, aligning with Trump’s calls for lower borrowing costsConference Board U.S. Leading Economic Index falls 0.3% in September, points to 2026 slowdownBroad Market Price Action:

Trump’s Politico interview raised fresh questions about tariff policy consistency, potentially supporting defensive dollar positioning. The greenback’s recovery seemed to correlate with renewed caution in equity markets and a modest uptick in Treasury yields, suggesting haven flows were reasserting themselves.

The U.S. session delivered choppy, mixed dollar performance with an arguably bearish lean through the afternoon. The JOLTS job openings data at 10:00 am ET came in well above expectations at 7.67 million versus 7.12 million forecast, which initially sparked a brief dollar bounce as the hawkish data suggested the labor market remained tighter than feared. However, analysts quickly noted the data’s limitations—it was stale, delayed by the government shutdown, and the pace of layoffs had also risen. This nuance seemed to temper the dollar’s gains, and the greenback drifted lower through the afternoon as traders likely returned focus to Wednesday’s Fed meeting.

Upcoming Potential Catalysts on the Economic Calendar

- Japan Reuters Tankan Index for December 2025 at 11:00 pm GMT

- Japan Producer Prices Index for November 2025 at 11:50 pm GMT

-

China Inflation Updates for November 2025 at 1:30 am GMT

- Euro area ECB President Lagarde Speech at 10:55 am GMT

- U.S. MBA 30-Year Mortgage Rate & Applications for December 5, 2025 at 12:00 pm GMT

- U.S. Wholesale Inventories Adv for September 2025

- U.S. Employment Cost Index for September 2025 at 1:30 pm GMT

- U.S. Wholesale Inventories Adv for October 2025

-

Bank of Canada Interest Rate Decision for December 10, 2025 at 2:45 pm GMT

- BoC Press Conference at 3:30 pm GMT

- EIA Crude Oil Stocks Change for December 5, 2025 at 3:30 pm GMT

-

FOMC Federal Funds Rate statement for December 10, 2025 at 7:00 pm GMT

-

FOMC Economic Projections at 7:00 pm GMT

-

Fed Press Conference at 7:30 pm GMT

Wednesday’s calendar is dominated by two major central bank decisions that will shape near-term market direction. The Federal Reserve is widely expected to deliver a 25-basis-point cut—the market prices this with nearly 90% probability—but the real focus will be on Powell’s guidance for 2026. Money markets have already retreated from optimistic forecasts, now pricing around two cuts next year versus more aggressive expectations just weeks ago. The key risk is a “hawkish cut” where the Fed lowers rates but signals a pause in the easing cycle, which could trigger volatility across assets. As one strategist noted, “the rate cut is actually the least important part of this meeting”—the updated dot plot and Powell’s commentary on the labor market, inflation trajectory, and policy path will carry far more weight.

The Bank of Canada decision at 2:45 pm GMT adds another layer of intrigue, with all 13 economists surveyed expecting rates to hold steady at 3.75%. However, recent pricing of a late-2026 rate hike has tightened Canadian financial conditions, potentially prompting Governor Macklem to push back with more dovish guidance at his 4:00 pm GMT press conference.

China’s inflation data overnight will be watched for signs of deflation persistence, though unless we see major surprises, the reports are unlikely to move markets significantly given the focus on North American central banks.

The combination of Fed projections, Powell’s press conference language around the January meeting, and any BOC commentary on rate hike expectations could drive significant moves in bonds, the dollar, and equity volatility—particularly if either central bank surprises relative to the cautious tone markets are now pricing.

Stay frosty out there, forex friends, and don’t forget to check out our Forex Correlation Calculator when planning to take on risk!

Overlay of USD vs. Majors Forex Chart by TradingView