Unexpected Market Moves on October 21, 2025: What Traders Aren’t Telling You

Ever wonder how markets keep their cool when everything else seems to be on a rollercoaster? Tuesday proved just that—equities hovering near record highs while precious metals took a nosedive. It’s like watching a tightrope walker juggle flaming torches—impressive, but nerve-wracking. Meanwhile, the UK and Canada are throwing mixed signals that make central bank strategies feel like a chess game with invisible pieces. Toss in some surprising inflation data and innovative Fed technology talk, and you’ve got a cocktail that’ll keep traders on their toes. Curious what that means for your portfolio or the forex world? Dive into the latest twists and turns you might’ve missed in this electric session. LEARN MORE.

Markets displayed resilience on Tuesday as equity indices held near record highs despite a sharp selloff in precious metals, while mixed economic signals from the UK and Canada highlighted diverging central bank challenges ahead of key inflation data.

Check out the forex news and economic updates you may have missed in the latest trading session!

Headlines & Data:

- New Zealand Credit Card Spending for September 2025: 0.2% (3.7% forecast; 3.5% previous)

- Swiss Balance of Trade for September 2025: 2.8B (3.2B forecast; 3.9B previous)

- U.K. Public Sector Net Borrowing Ex Banks for September 2025: -20.2B (-15.2B forecast; -17.96B previous)

- European Central Bank’s chief economist Philip Lane said on Tuesday that Eurozone banks may come under pressure if US dollar funding were to dry up

-

Canada Consumer Price Index Growth Rate for September 2025: 0.1% m/m (-0.1% m/m forecast; -0.1% m/m previous); 2.4% y/y (2.2% y/y forecast; 1.9% y/y previous)

- Canada Core Inflation Rate for September 2025: 0.2% m/m (0.1% m/m forecast; 0.0% m/m previous); 2.8% y/y (2.7% y/y forecast; 2.6% y/y previous)

- Federal Reserve Governor Waller said on Tuesday that the Fed will increase its look into innovative technology in payments

- New Zealand Global Dairy Trade Price Index for October 21, 2025: 21.9% (-0.7% forecast; -1.6% previous)

Broad Market Price Action:

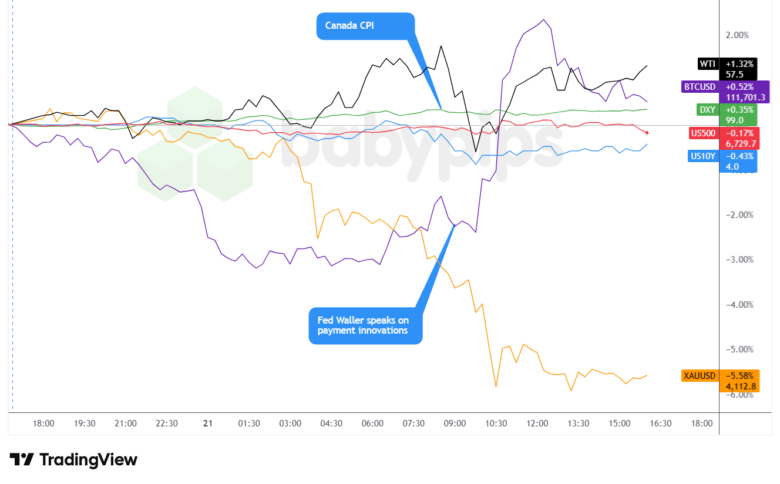

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Tuesday’s trading session saw Wall Street maintain positions near all-time highs following the S&P 500’s recent strong performance, with the benchmark index fluctuating around 6,730. Industrial firms including General Electric Co. and 3M Co. paced gains, while technology sector attention focused on OpenAI’s announcement of its first AI-powered web browser.

Gold and silver experienced their biggest slide in years, retreating from successive record highs. The precious metals selloff reflected a confluence of factors including positive US-China trade developments, a stronger dollar, and overstretched technical indicators. Gold’s rally in recent months had been fueled by falling yields, persistent central bank buying, and expectations of further monetary easing.

WTI crude oil traded mostly net positive for the day, possibly supported by news of the U.S. seeing to buy 1 million barrels of oil for the Strategic Petroleum Reserve, creating instant demand for oil.

Bitcoin bounced higher, recovering from earlier session weakness to trade above $114,000 momentarily, though remaining well below its early October record high of $126K. The pop higher during the U.S. session shortly follows Federal Reserve Governor Waller’s comments on innovations in payments technology, potentially supporting the likely move into blockchain technology to support payment systems.

Treasury 10-year yields fell two basis points to 3.96%, continuing their decline as markets priced in expectations for further Federal Reserve rate cuts. The yield curve movement suggested investors remain focused on the Fed’s next policy decision scheduled for October 29.

The S&P 500 remained near record territory despite elevated valuations and ongoing economic uncertainties. Markets have defied warnings over the past six months, clocking one of the best stretches since the 1950s.

FX Market Behavior: U.S. Dollar vs. Majors:

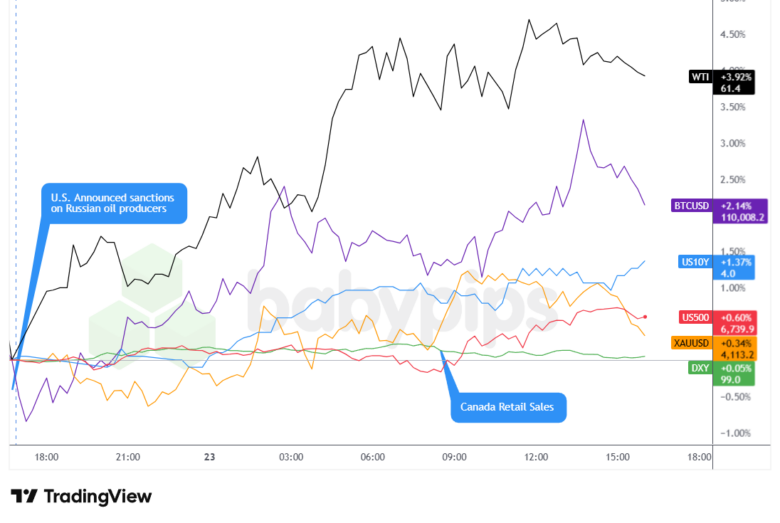

Overlay of USD vs. Majors Chart by TradingView

The U.S. dollar posted mixed performance on Tuesday, exhibiting initial weakness before recovering to close the session with gains against most major currencies, with the notable exception of the Canadian dollar which strengthened on hotter-than-expected inflation data.

The greenback experienced a slight dip during early Asian trading hours before mounting a rally through the remainder of the Asian session and the London session. This was likely on improving U.S.-China trade developments seen in the past few days, and easing concerns about US regional bank credit quality (Zions Bancorp reporting profits that topped estimates despite a $50 million loss from an alleged fraud incident).

During the U.S. trading session, when the dollar traded net bearish initially before staging a modest rebound ahead of the day’s close, likely reflecting the net positive shift in broad risk sentiment, and possible flows from gold back to U.S. assets like bonds and the greenback.

USD/CAD emerged as the day’s clear outlier, with the Canadian dollar strengthening notably following the release of September inflation figures. Canadian headline inflation accelerated to an annual rate of 2.4% in September from 1.9% in August, above the 2.2% forecast, marking the highest level in seven months and the first time in six months that inflation exceeded the Bank of Canada’s 2% target.

Upcoming Potential Catalysts on the Economic Calendar

- Japan Balance of Trade for September 2025 at 11:50 pm GMT

- Japan BoJ JGB Purchase at 3:35 am GMT

- U.K. Inflation Growth Rate updates for September 2025 at 6:00 am GMT

- Euro area ECB Guindos Speech at 11:00 am GMT

- U.S. MBA 30-Year Mortgage Rate & Mortgage Applications for October 17, 2025 at 11:00 am GMT

- Euro area ECB President Lagarde Speech at 12:25 pm GMT

- U.S. EIA Crude Oil Stocks Change for October 17, 2025 at 2:30 pm GMT

- U.K. BoE Woods Speech at 8:00 pm GMT

Wednesday’s calendar centers on UK inflation data for September, which could significantly impact gilt markets and sterling given the already-fragile state of British public finances ahead of Chancellor Rachel Reeves’ November 26 budget.

Speeches from ECB President Lagarde and Vice President Guindos may provide some euro volatility with any shift in the central bank’s policy stance, particularly in light of concerns about eurozone bank funding conditions raised by Chief Economist Lane. Developments in US-China trade negotiations following positive signals from both sides will remain a key focus for broader market sentiment.

Any fresh commentary on the ongoing US government shutdown could drive volatility, particularly if there are signs of progress toward resolution. The combination of these factors if they arise significantly raises the potential for increased market activity across forex pairs and broader asset classes.

Stay frosty out there forex friends and don’t forget to check out our Forex Correlation Calculator when taking any trades!

Post Comment