Why Your Deals Are Influenced Before Your Reps Even Enter the Room

Ninety-four percent of buying groups select their preferred vendor before interacting with any salesperson, and that chosen vendor wins about 80% of the time. These statistics from the 2025 Buyer Experience Report highlight that decisions are typically made before sales representatives engage.

This means the discovery call sales reps prepare for is not the initial meeting. Research indicates vendors are involved late in the process, primarily to confirm a decision the buying group has already made.

The decisive phase has shifted. Now, 51% of B2B software buyers begin their research by consulting AI chatbots—nearly double the 29% who did so just months prior. Others rely on peer reviews and private communities of similar professionals.

This article explores the unseen half of the buying process: how early decisions occur, where buyers develop their opinions, and why traditional pipeline strategies underperform.

TL;DR

- The buying journey is divided into a lengthy, invisible research phase and a brief validation phase; most decisions happen during the unseen portion without seller involvement.

- AI assistants and peer reviews serve as buyers’ true first meeting, setting shortlists and highlighting vendors’ strengths before any salesperson interaction.

- The supporting evidence for these decisions is timely and authored by informed buyers across major software categories.

- Conventional pipeline tactics falter as they disrupt buyers instead of engaging where decisions are actually made.

- Most pipeline losses stem from visibility issues, not insufficient effort; increasing activity cannot resolve a lack of presence.

Why Are B2B Deals Decided Before Sales Reps Get Involved?

B2B deals conclude early because the buying journey consists of two parts, with sales teams only witnessing the latter. The initial phase is lengthy, quiet, and self-directed—buyers research, compare, and seek advice independently. By the time demos and discovery discussions occur, most critical evaluations are complete. Kerry Cunningham of 6sense states, “Buyers are choosing a preliminary winner much earlier than they have in the past.”

G2’s research confirms this trend: about two-thirds of buyers involve salespeople only in the later purchase stages. Sales conversations are scheduled after the shortlist exists.

Moreover, decisions form faster with AI tools, as noted in G2’s Answer Economy report where 80% of buyers agreed AI accelerated their choices, leaving little influence opportunity once reps engage.

Where Do Buyers Form Opinions Before Talking to Sales?

Buyers develop opinions early in three interconnected places:

- AI assistants

- Peer review platforms

- Private communities of peers

Ninety-four percent of buying groups have already picked their preferred vendor before they speak to a single salesperson. That favorite goes on to win about 80% of the time.

Both numbers come from the 2025 Buyer Experience Report, and together they say the same thing: the deal is usually decided before your reps enter the room.

That means the discovery call your rep is preparing for is not a first meeting. The same research found that vendors are now pulled in near the end of the journey, largely to validate a choice the buying group has already made.

And the phase that decides everything has changed hands. Half of B2B software buyers (51%) now start their research by asking an AI chatbot, nearly double the 29% who did just months earlier. The rest lean on peer reviews and on private communities of people like them.

This article maps the half of the deal you cannot see: how early it gets decided, where buyers actually form their opinions, and why the standard pipeline playbook keeps underperforming against it.

TL;DR

- The buying journey has split into a long, invisible research phase and a short validation phase. Most of the decision now happens in the invisible part, where sellers are absent.

- AI assistants and peer reviews have become the buyer’s real first meeting. Together, they set the shortlist and frame your strengths before anyone on your team says a word.

- The evidence layer behind those answers is current and written by serious buyers, and it exists in every major software category.

- Traditional pipeline plays are decaying because they interrupt buyers instead of showing up where decisions actually form.

- Most pipeline declines are visibility problems misdiagnosed as effort problems. More activity cannot fix an absence.

Why are B2B deals decided before sales reps get involved?

B2B deals get decided early because the buying journey has split into two halves, and sales teams only ever see the second one.

The first half is long, quiet, and self-directed. Buyers read, compare, ask around, and form conclusions without filling in a form or taking a call. By the time the second half starts, the one with demos and discovery questions, most of the heavy thinking is done. Kerry Cunningham, who leads the 6sense research behind those opening numbers, put it plainly: “Buyers are choosing a preliminary winner much earlier than they have in the past.”

G2’s own buyer research shows the same pattern. In the 2025 Buyer Behavior Report, roughly two-thirds of buyers said they bring salespeople in only during the later stages of the purchase. The journey is not missing a sales conversation. The sales conversation is scheduled for the end, after the shortlist already exists.

The window is shrinking, too. In G2’s Answer Economy research, four out of five buyers said AI tools sped up their purchase decisions. So, while decisions form in the invisible part, they are forming fast there, leaving even less room to influence anything once you finally get the call.

Where do buyers form their opinions before they ever talk to sales?

Buyers form their opinions in three connected places long before a discovery call:

- AI assistants

- Peer review platforms

- Private communities of colleagues and operators.

However, sellers don’t have direct visibility into any of them.

The AI layer is growing fastest, and its answers carry real decision weight. Beyond the 51% who now start their research there, 69% of buyers chose a different vendor than the one they originally had in mind because of what an AI told them. And one in three bought from a vendor they had never heard of before an AI surfaced it.

Tim Sanders, G2’s Chief Innovation Officer, describes the shift bluntly: The funnel buyers used to walk through step by step is collapsing, because “AI chatbots are compressing it into a single answer.” If your brand is not in that answer, the buyer’s first impression of you is your absence.

Relative influence has shifted as well. When G2 asked enterprise buyers which sources they actually use, review platforms came out on top at 56%, with AI search right behind at 55%. And when buyers ranked what shapes the shortlist itself, AI assistants scored 17.1%, review platforms 15.1%, and salespeople 8.8%.

A salesperson now carries roughly half the shortlist influence of a chatbot.

The two layers are not separate, either. AI assistants build their answers largely out of peer evidence. When growth advisor Kevin Indig analyzed 30,000 AI citations for G2, review platforms emerged as core source material, with G2 the most cited software review source at a 22.4% share of voice among review sites.

His companion analysis found the relationship is roughly linear: “A 10% increase in reviews correlates with a 2% increase in citations.” The machine’s answer is, to a meaningful degree, a compression of what your customers wrote.

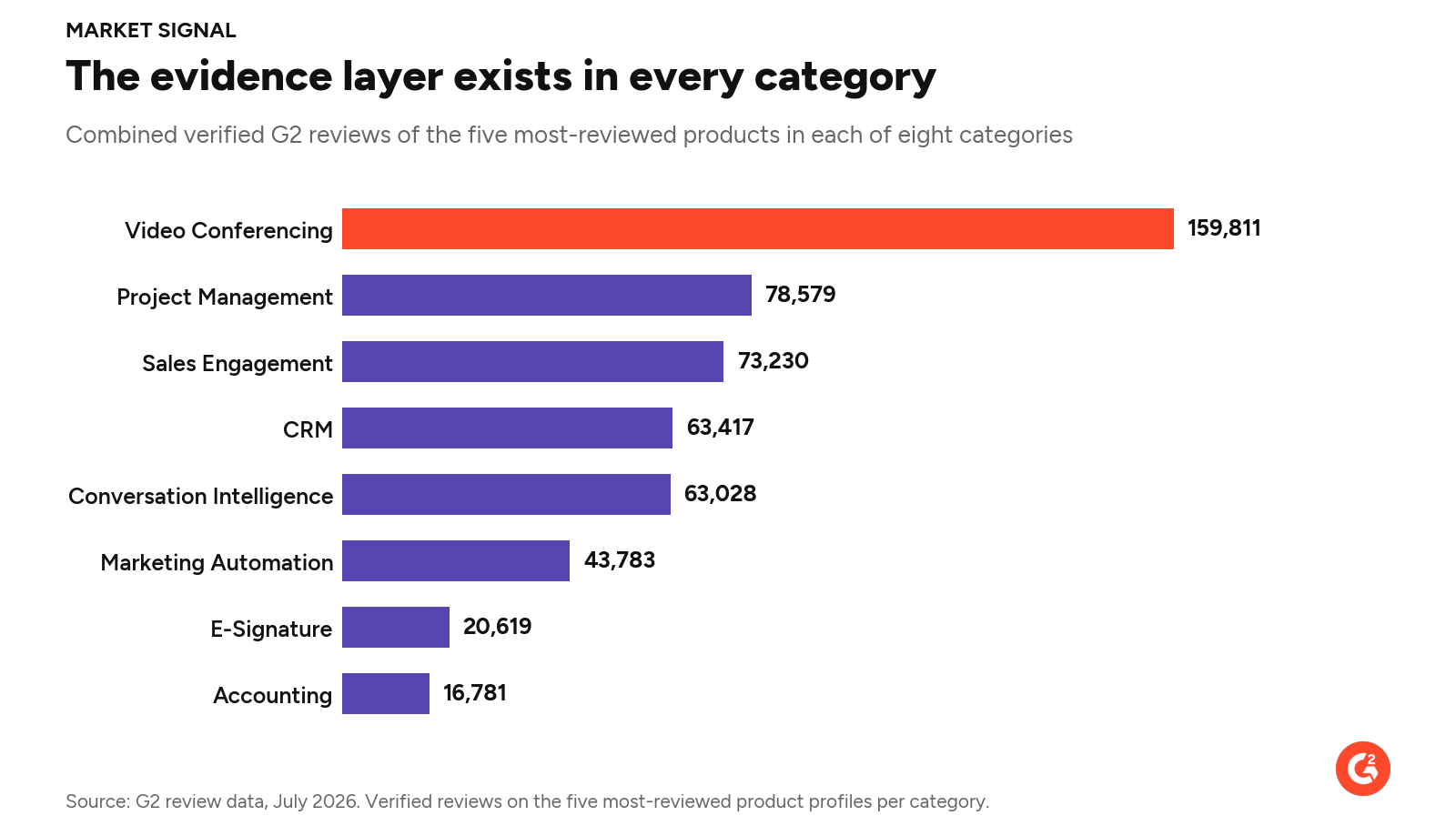

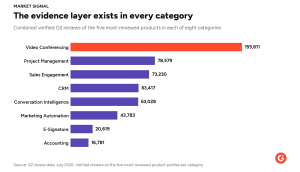

It is fair to ask how big this evidence layer really is.

So we measured it. On July 7, 2026, we pulled G2 review data for the five most-reviewed products in eight software categories, chosen to span the whole business stack: CRM, sales engagement, conversation intelligence, marketing automation, project management, accounting, e-signature, and video conferencing.

Volume alone would not matter if the reviews came from hobbyists. They do not. We went one level deeper on six of those category leaders, one per category, and each from a different vendor: Agentforce Sales, HubSpot Marketing Hub, Smartsheet, NetSuite, Zoom Workplace, and Gong.

Pooled across their 129,429 reviews that carry company-size data, 61% come from people at companies with more than 50 employees. The share runs from 47% at HubSpot Marketing Hub to 87% at Gong, and even the low end means nearly half the voices are mid-market and enterprise.

The roles of reviewers matter as much as the volume: Across those six products, the reviewer base includes 33,855 administrators, 7,394 consultants, and 2,507 executive sponsors. These are the people who run this software, implement it, and are part of the buying committees.

And the shelf restocks itself daily. The same six products added 11,438 new verified reviews in the 12 months. This was from July 2025 to July 2026, and about 31 every single day. Even the slowest of the six, Gong at 559, means a fresh peer verdict landing in its category more than 10 times a week.

One more fact about who is doing the reading: Across G2, 80% of product profiles are now cited by AI systems more often than they are viewed by humans.

Whatever category you sell in, recent peer evidence exists. Buyers consult it directly, and AI engines compile it into answers where your buyers research.

How much do G2 reviews actually influence enterprise software buying decisions?

G2 reviews now carry more weight with enterprise software buyers than any channel a vendor controls. Enterprise buyers rank review sites as their single most-used research source, and reviews outrank vendor websites, analyst firms, and salespeople when shortlists get built.

Enterprise buyers report this. In G2’s survey of 1,100 B2B decision-makers, enterprise buyers named review sites their top research source at 56%, just ahead of AI search at 55%. Among small-business buyers, those figures drop to 38% and 35%. That contrast inverts a common assumption: Peer reviews are not a small-company shortcut that enterprises outgrow. The bigger the company, the more the buying committee leans on them.

The influence question gets even more direct. When those same buyers ranked what shapes their vendor shortlist, software review sites scored 15.1%, ahead of vendor websites at 12.8%, market research firms at 10.6%, peers and colleagues at 8.9%, and salespeople at 8.8%.

AI assistants assemble answers from review content; a review’s reach now extends far beyond the people who open the page.

Why is the traditional pipeline playbook no longer enough?

The traditional pipeline playbook struggles now because it was built on an assumption that quietly stopped being true: that a seller can start the conversation.

Look at what interruption actually returns. Belkins analyzed 7.5 million cold emails sent in 2025 and found an average reply rate of 0.45%. At companies with more than 10,000 employees, the exact accounts most enterprise teams are paid to crack, the average reply rate falls to 0.22%. That is roughly one reply for every 450 emails, and a reply is not a meeting, let alone a deal.

The decay shows up at the bottom of the funnel as well. Benchmarks from Ebsta and Pavilion show average B2B win rates falling from 29% to 19%. The same body of research points to timing as the lever that still works: Deals where sellers reached decision makers early showed roughly a 55% lift in win rates. The problem is that the old playbook almost never gets you in early, because “early” now happens inside a phase you cannot see.

That is the structural flaw. Cold outreach lands either too early, before any active need exists, or too late, after the reading room has reached its verdict.

And since sellers are engaged mainly to validate, the responses you do get skew toward buyers who have already decided, often for someone else.

What are the real causes of pipeline decline?

Most pipeline declines trace back to visibility problems, not effort problems, which is why working harder at the old playbook so rarely fixes them. Four root causes show up repeatedly:

The absence from AI answers

If AI assistants describe your category without naming you, and your review presence is thin where competitors’ run deep, buyers act on the data: They form a shortlist you are not on and never tell you. We have written before about how your best buyers disqualify you without saying a word. The deals you lose this way never show up as losses, but show up as silence.

A compounding evidence gap

The velocity numbers above are the uncomfortable part. Category leaders add fresh peer proof every day, about 31 reviews daily across just six products, so standing still means falling behind on the material both humans and AI engines use to judge you. A stale profile reads as a risk to a buyer and as nothing at all to a machine assembling an answer.

Misread silence

An account with no opens, no replies, and no form fills is not necessarily an account with no activity. It is often an account doing what two-thirds of buyers now do. They research thoroughly and plan to surface at the end. Quiet pipelines and dead pipelines look identical in a CRM, and teams keep treating the first like the second.

Measurement built for the old journey

MQLs and sequence touches aren’t the end of measuring. The dashboard stays green while the shortlist forms somewhere else. That is how a visibility problem gets diagnosed as an effort problem.

None of this means outbound is dead or that reps stopped mattering. It means the decision moved upstream, into a research phase that relies on AI-generated answers and peer-reviewed evidence.

The 94% who arrive with a favorite have already met you, through a chatbot’s summary and a few hundred of your customers’ reviews, whether you showed up well or not at all.

If you want to gauge your AI search visibility, take this audit from part one of this series.

Post Comment