Unexpected Market Shifts on April 16, 2026: What Traders Need to Know Now

So here we are again, witnessing the markets just not wanting to quit—breaking records like it’s their day job. Now, add to that a surprise 10-day Israel-Lebanon ceasefire announcement by President Trump and a jaw-dropping 58% quarterly profit leap from TSMC. Could it be that geopolitical calm and semiconductor brilliance are the ultimate cocktail for this rally? The S&P 500 didn’t just dip a toe; it splashed right into a new all-time closing high. Meanwhile, the U.S. dollar gave most majors a run for their money, except the Canadian dollar, who apparently had other plans. If you thought the week’s trading news was just noise, think again—there’s a delicious mix of economic reports and market moves you don’t want to miss. Ready to dive deeper and unravel what’s really driving these market grooves?

Markets extended their record-breaking run on Thursday as President Trump announced a 10-day Israel-Lebanon ceasefire and TSMC posted a 58% jump in quarterly profit, providing both geopolitical and fundamental fuel for the rally. The S&P 500 logged another all-time closing high while the U.S. dollar finished as one of the session’s better-performing major currencies, gaining against all majors except the Canadian dollar.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Australia Consumer Inflation Expectations for April 2026: 5.9% (5.4% forecast; 5.2% previous)

- Australia Employment Change for March 2026: 17.9k (34.2k forecast; 48.9k previous)

- China GDP Growth Rate for March 31, 2026: 5.0% y/y (5.2% y/y forecast; 4.5% y/y previous); 1.3% q/q (1.4% q/q forecast; 1.2% q/q previous)

- China Retail Sales for March 2026: 1.7% y/y (3.5% y/y forecast; 2.8% y/y previous)

- China Unemployment Rate for March 31, 2026: 5.4% (5.2% forecast; 5.3% previous)

- China Industrial Production for March 2026: 5.7% y/y (5.4% y/y forecast; 6.3% y/y previous)

- U.K. Manufacturing Production for February 2026: -0.5% y/y (-0.5% y/y forecast; 1.3% y/y previous); -0.1% m/m (0.1% m/m forecast; 0.1% m/m previous)

- U.K. GDP for February 2026: 1.0% y/y (1.0% y/y forecast; 0.8% y/y previous)

- Swiss Producer & Import Prices for March 2026: -2.7% y/y (-0.2% y/y forecast; -2.7% y/y previous); 0.2% m/m (0.2% m/m forecast; -0.3% m/m previous)

- SNB Monetary Policy Meeting Minutes: The minutes show the SNB keeping its policy rate at 0%, judging overall monetary conditions as having tightened due to Swiss franc appreciation and seeing its conditional inflation forecast still within the price stability range and very close to the previous quarter’s path.

-

Euro area CPI Growth Rate Final for March 2026: 2.6% y/y (2.5% y/y forecast; 1.9% y/y previous)

- Euro area Core Inflation Rate Final for March 2026: 2.3% y/y (2.3% y/y forecast; 2.4% y/y previous)

- Canada New Motor Vehicle Sales for February 2026: 124.0k (80.0k forecast; 114.41k previous)

- U.S. Initial Jobless Claims for April 11, 2026: 207.0k (216.0k forecast; 219.0k previous)

- U.S. NY Fed Services Activity Index for April 2026: -14.0 (-22.6 previous)

- Philadelphia Fed Manufacturing Index for April 2026: 26.7 (17.0 forecast; 18.1 previous)

- U.S. Industrial Production for March 2026: 0.7% y/y (1.8% y/y forecast; 1.4% y/y previous)

- U.S. Manufacturing Production for March 2026: 0.5% y/y (2.0% y/y forecast; 1.3% y/y previous)

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

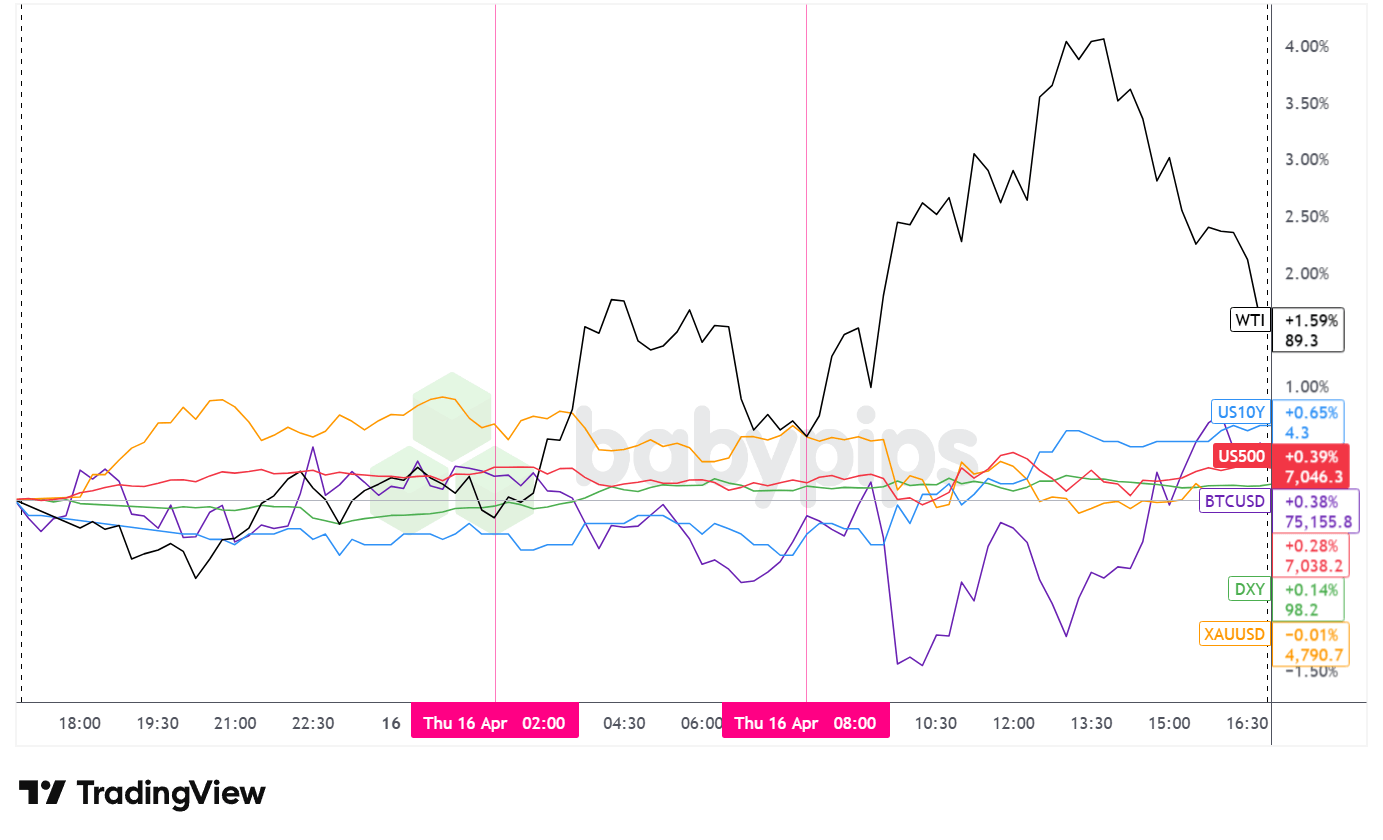

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Thursday delivered another constructive session for risk assets, with equities and oil extending gains against a backdrop of incremental geopolitical de-escalation and a powerful earnings beat from the semiconductor sector.

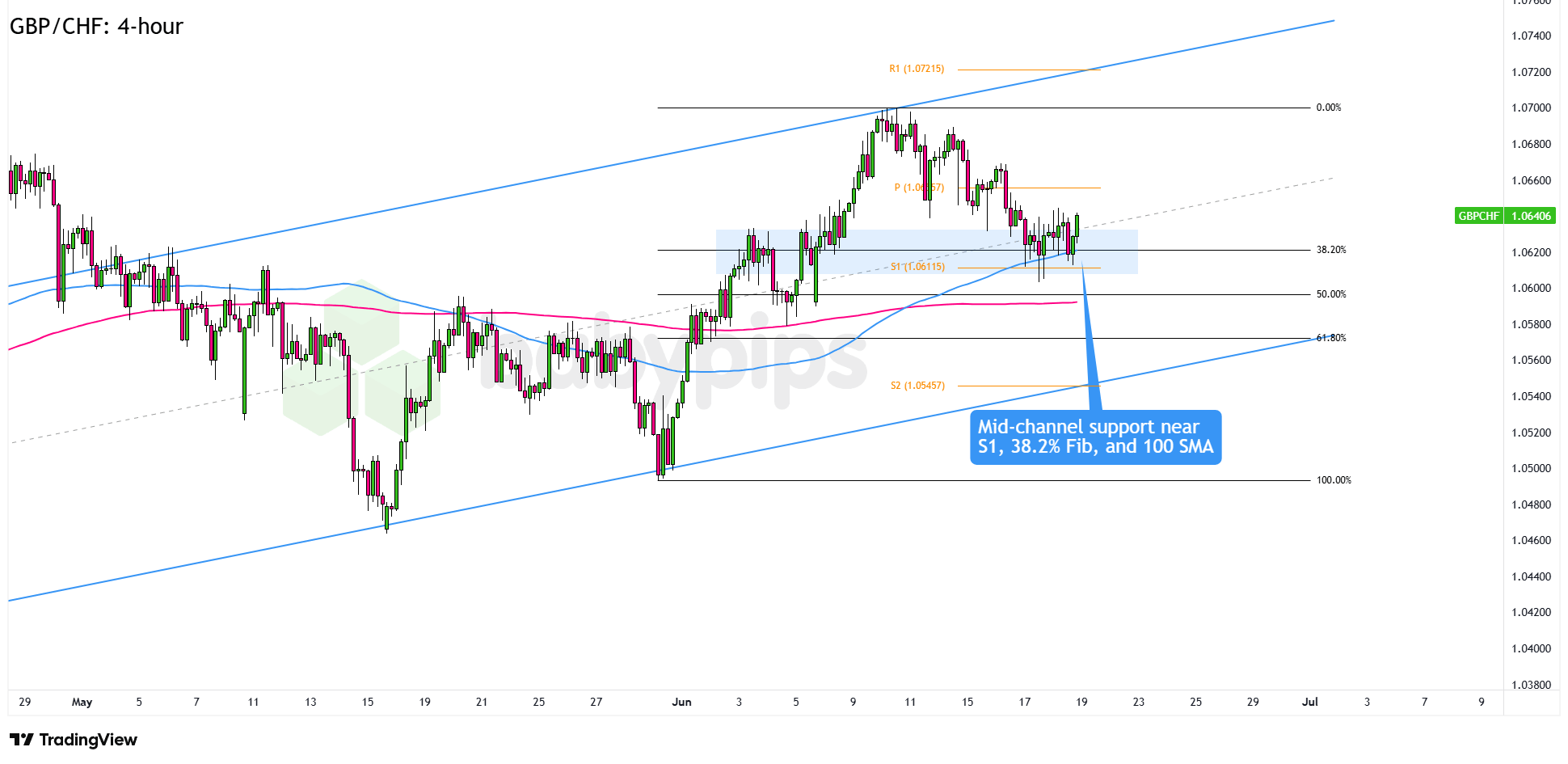

The S&P 500 closed at a fresh all-time high, gaining 0.39% to settle at 7,046.0. The index opened the U.S. session near flat before bearish pressure lower around the 10:30 AM ET mark brought price to an intraday low near 7,017. The index recovered swiftly, surging to an intraday high above 7,051 around midday before pulling back to close near 7,039. The intraday pattern appeared to reflect the digestion of a heavy simultaneous data slate, including Philly Fed and initial jobless claims, before bullish momentum resumed. The Nasdaq Composite logged its 12th consecutive positive session, its longest winning streak since July 2009, with technology shares continuing to benefit from TSMC’s blockbuster first-quarter earnings that validated the AI infrastructure investment thesis.

WTI crude oil was the session’s strongest performer among broad assets, advancing 159% to settle near $89.30 per barrel. The move was notable given the constructive geopolitical backdrop, suggesting that supply concerns tied to the ongoing U.S. naval blockade of the Strait of Hormuz likely continued to underpin crude prices even as the ceasefire framework slowly expanded. The rally began in the London session and extended into the U.S. morning, with price reaching a session high near $91.76 before easing into the close.

Gold declined slightly to settle near $4,790 per ounce. After an opening bump higher, the precious metal traded with relative stability through the Asian session before beginning a steady downtrend that accelerated after the U.S. session opened, touching an intraday low near $4,773. The move appeared broadly consistent with the session’s risk-on tone, as investor appetite for safe-haven assets likely eased alongside the equity rally and ceasefire headlines.

Bitcoin ended slightly positive for the day, gaining 0.38% to trade near $75,155. The cryptocurrency traded with notable intraday volatility, dipping sharply toward the $73,300 area in the early U.S. session before recovering firmly to close near its daily highs. The choppy action suggested crypto markets were sensitive to the same risk-on/risk-off swings seen across other asset classes throughout the session.

The U.S. 10-year Treasury yield rose approximately 0.79% on the day to settle near 4.31%. Yields were largely subdued through the Asian and London sessions but moved higher after the U.S. open, likely reflecting the Philly Fed’s significant beat on manufacturing and the strong new orders sub-index, alongside the below-forecast initial jobless claims print, which may have nudged traders to temper near-term rate cut expectations modestly.

Promotion: If your confidence has grown in your market awareness & strategies with this market recap, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $13, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

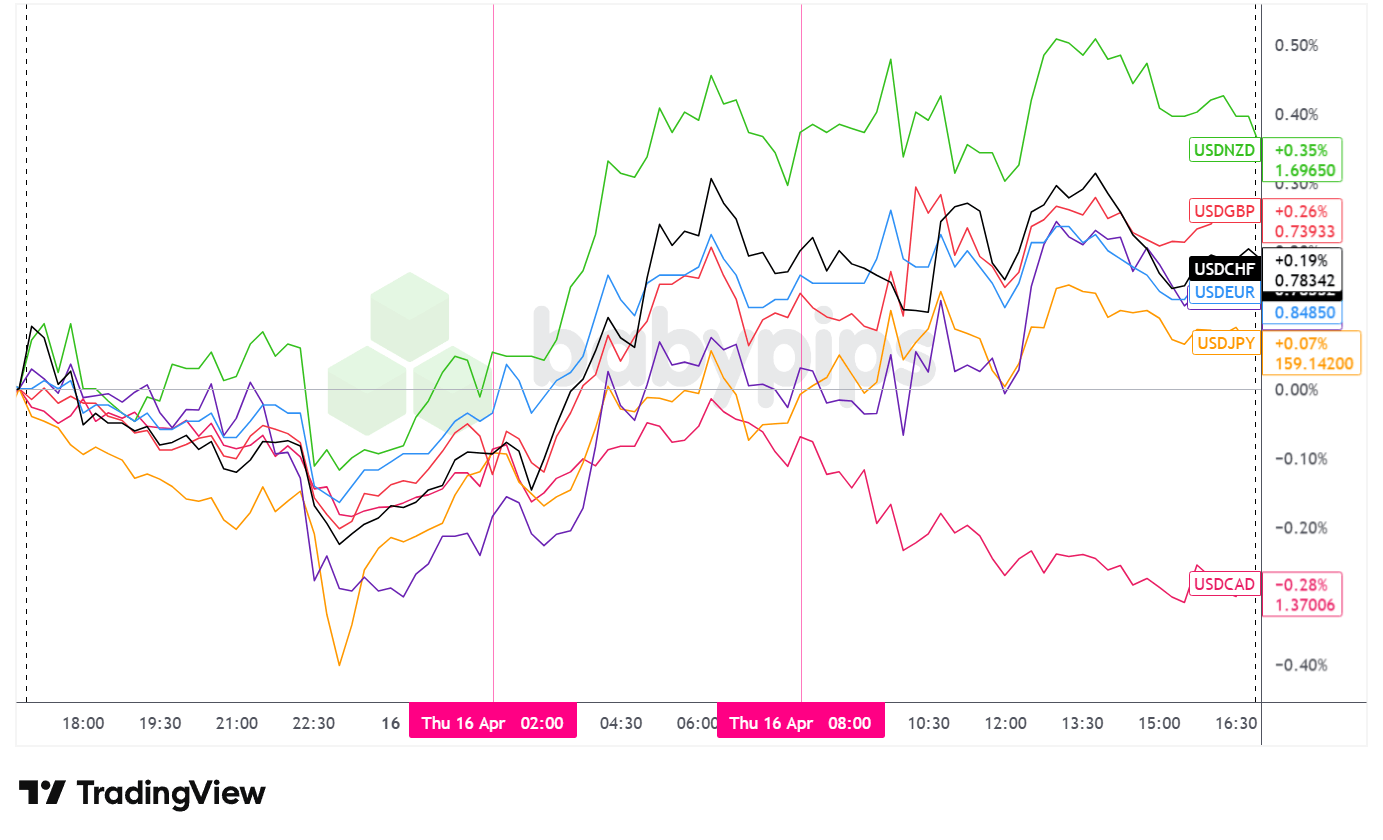

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar closed Thursday as one of the session’s better-performing major currencies, ending the day higher against all majors except the Canadian dollar. The intraday journey involved several distinct phases across the three main trading sessions.

During the Asian session, the dollar initially fell against the major currencies, likely reflecting the session’s tentative risk-on tone as Australia’s employment data and China’s GDP crossed the tape alongside ongoing Iran ceasefire optimism. The Aussie received a modest lift from the jobs report, which showed full-time employment surging 52.5k against a 20.0k forecast even as the headline employment change fell short of expectations, while China’s Q1 GDP growth of 5.0% year-over-year came in slightly below the 5.2% forecast. The dollar found a floor and began to stabilize, rebounding slightly as the session transitioned toward Europe. Japan Finance Minister Katayama’s warning of potential “bold action” in currency markets following talks with U.S. Treasury Secretary Bessent provided some firming pressure, nudging USD/JPY away from the 159 level.

During the London session, the dollar continued its rebound against most major currencies before topping out and pulling back slightly as the U.S. session approached. European data was broadly in line to modestly mixed, providing limited directional catalyst in isolation. The U.K. GDP print met expectations at 1.0% year-over-year, though manufacturing production continued to contract. Eurozone final CPI came in slightly above the preliminary reading at 2.6% year-over-year, with core inflation holding at 2.3%. The ECB published its monetary policy meeting accounts during this window, though no material market reaction appeared to accompany the release. Swiss National Bank meeting minutes reiterated the policy rate at 0% and flagged the franc’s safe-haven appreciation as a de facto tightening of monetary conditions. The SNB’s cautious tone may have tempered some franc demand at the margin.

After the U.S. session opened, the dollar traded with elevated intraday volatility, swinging in both directions before settling into a net positive posture for the remainder of the session. The Philly Fed Manufacturing Index for April delivered a strong upside surprise at 26.7 against the 17.0 forecast, with new orders surging to 33.0 from 8.6 and prices paid jumping to 59.3, pointing to accelerating activity alongside building input cost pressures. Initial jobless claims fell to 207k against a 216k forecast, suggesting the labor market remains resilient. These two releases likely provided the fundamental backdrop that allowed the dollar to firm through the afternoon. The sharp miss in U.S. industrial production for March at -0.5% month-over-month against a +0.5% forecast was a counterpoint, though markets appeared to give greater weight to the forward-looking Philly Fed data.

Upcoming Potential Catalysts on the Economic Calendar

- Australia Consumer Inflation Expectations for April 2026 at 1:00 am GMT

- Australia Employment Situation Update for March 2026 at 1:30 am GMT

- China GDP Growth Rate for March 31, 2026 at 2:00 am GMT

- China Unemployment Rate for March 31, 2026 at 2:00 am GMT

- China Industrial Production for March 2026 at 2:00 am GMT

- China Retail Sales for March 2026 at 2:00 am GMT

- ECB Lane Speech at 3:40 am GMT

- U.K. Manufacturing & Industrial Production for February 2026 at 6:00 am GMT

- U.K. GDP for February 2026 at 6:00 am GMT

- Swiss Producer & Import Prices for March 2026 at 6:30 am GMT

- SNB Monetary Policy Meeting Minutes at 7:30 am GMT

- Euro area CPI Growth Rate Final for March 2026 at 9:00 am GMT

- ECB Monetary Policy Meeting Accounts at 11:30 am GMT

- Canada New Motor Vehicle Sales for February 2026 at 12:30 pm GMT

- U.S. Philadelphia Fed Manufacturing Index for April 2026 at 12:30 pm GMT

- U.S. NY Fed Services Activity Index for April 2026 at 12:30 pm GMT

- U.S. Initial Jobless Claims for April 11, 2026 at 12:30 pm GMT

- Fed Williams Speech at 12:35 pm GMT

- ECB Schnabel Speech at 1:00 pm GMT

- U.S. Industrial & Manufacturing Production for March 2026 at 1:15 pm GMT

Friday’s calendar is lighter on tier-one data, but Fed speakers Barkin and Waller could offer meaningful market-moving commentary given the week’s mixed signals: strong Philly Fed activity versus a soft industrial production print, and continued labor market resilience running alongside still-elevated inflation risk. Any remarks on the path of rate cuts, or the degree to which the Iran conflict’s energy price impact is influencing the Fed’s inflation outlook, will likely draw trader attention.

On the geopolitical front, the durability of both the U.S.-Iran ceasefire framework and the newly announced Israel-Lebanon ceasefire will remain the dominant macro variable heading into the weekend, with oil pricing likely to remain sensitive to any headline developments on either front.

Stay frosty out there, forex friends!

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

In “Unknown Market Wizards,” (⭐ 4.6★ | 1,400+ reviews on Amazon) Jack Schwager interviews successful traders to reveal a common truth: their edge isn’t just knowledge or skills—it’s their psychological resilience and rigid risk control. Whether you’re navigating shifting geopolitical themes or top tier economic data, learn how the “wizards” stay clinical when the rest of the market is emotional.

Master Your Trading Mindset with Market Wizards!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.