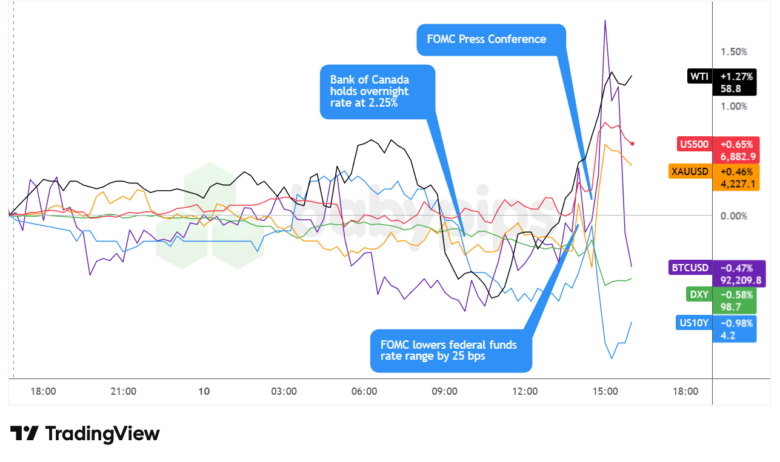

So, the Federal Reserve just dropped its third consecutive rate cut – not exactly a surprise but definitely a move that sparked quite a frenzy. Jerome Powell’s little nugget about tariffs causing only “transitory inflation” and the labor market holding stead? Well, that seemed to soothe the nerves more than the divided 9-3 FOMC vote or the modest 2026 rate cut outlook. Meanwhile, the Bank of Canada’s standstill on rates only adds fuel to the idea that the big central banks are nearing the finish line of their cutting marathon, thanks to some stubbornly resilient growth. You might be wondering how this all shakes out for your portfolios, currencies, and maybe even your next cup of coffee pricing. Intrigued? Buckle up — there’s plenty to unpack from the latest forex headlines to the broad market reactions that had traders riding a rollercoaster. LEARN MORE.

Swiss National Bank rate decision at 8:30 am GMT represents the day’s most significant scheduled catalyst, with markets closely watching whether the SNB will follow the Fed’s cautious approach or signal more aggressive easing given Switzerland’s proximity to zero inflation. Following the ECB’s recent hawkish commentary about rates potentially staying at current levels, any SNB divergence could drive meaningful franc volatility.

The Australian employment report at 12:30 am GMT could set the tone for Asian trading, with recent strength in labor markets potentially influencing RBA rate cut expectations. Any significant deviation from consensus could impact AUD positioning ahead of the European session.

U.S. Initial Jobless Claims at 1:30 pm GMT take on heightened importance following Chair Powell’s emphasis on labor market stabilization as a key rationale for Wednesday’s rate cut. With the government shutdown having delayed October and November employment data, weekly claims represent the most timely labor market signal available. A significant rise in claims could reignite concerns about labor market deterioration that Powell sought to address, potentially supporting further dollar weakness and reinforcing rate cut expectations.

Markets may trade cautiously as participants digest Wednesday’s divided FOMC vote and Powell’s nuanced messaging about the Fed being “well positioned to wait” before additional moves, suggesting a higher bar for January action. Fresh commentary from central bankers—including the BoE’s Kroszner—could provide additional color on the global rate outlook as policymakers across developed markets signal increasing caution about further easing.

Stay frosty out there, forex friends, and don’t forget to check out our Forex Correlation Calculator when planning to take on risk!

The Australian employment report at 12:30 am GMT could set the tone for Asian trading, with recent strength in labor markets potentially influencing RBA rate cut expectations. Any significant deviation from consensus could impact AUD positioning ahead of the European session.

U.S. Initial Jobless Claims at 1:30 pm GMT take on heightened importance following Chair Powell’s emphasis on labor market stabilization as a key rationale for Wednesday’s rate cut. With the government shutdown having delayed October and November employment data, weekly claims represent the most timely labor market signal available. A significant rise in claims could reignite concerns about labor market deterioration that Powell sought to address, potentially supporting further dollar weakness and reinforcing rate cut expectations.

Markets may trade cautiously as participants digest Wednesday’s divided FOMC vote and Powell’s nuanced messaging about the Fed being “well positioned to wait” before additional moves, suggesting a higher bar for January action. Fresh commentary from central bankers—including the BoE’s Kroszner—could provide additional color on the global rate outlook as policymakers across developed markets signal increasing caution about further easing.

Stay frosty out there, forex friends, and don’t forget to check out our Forex Correlation Calculator when planning to take on risk!