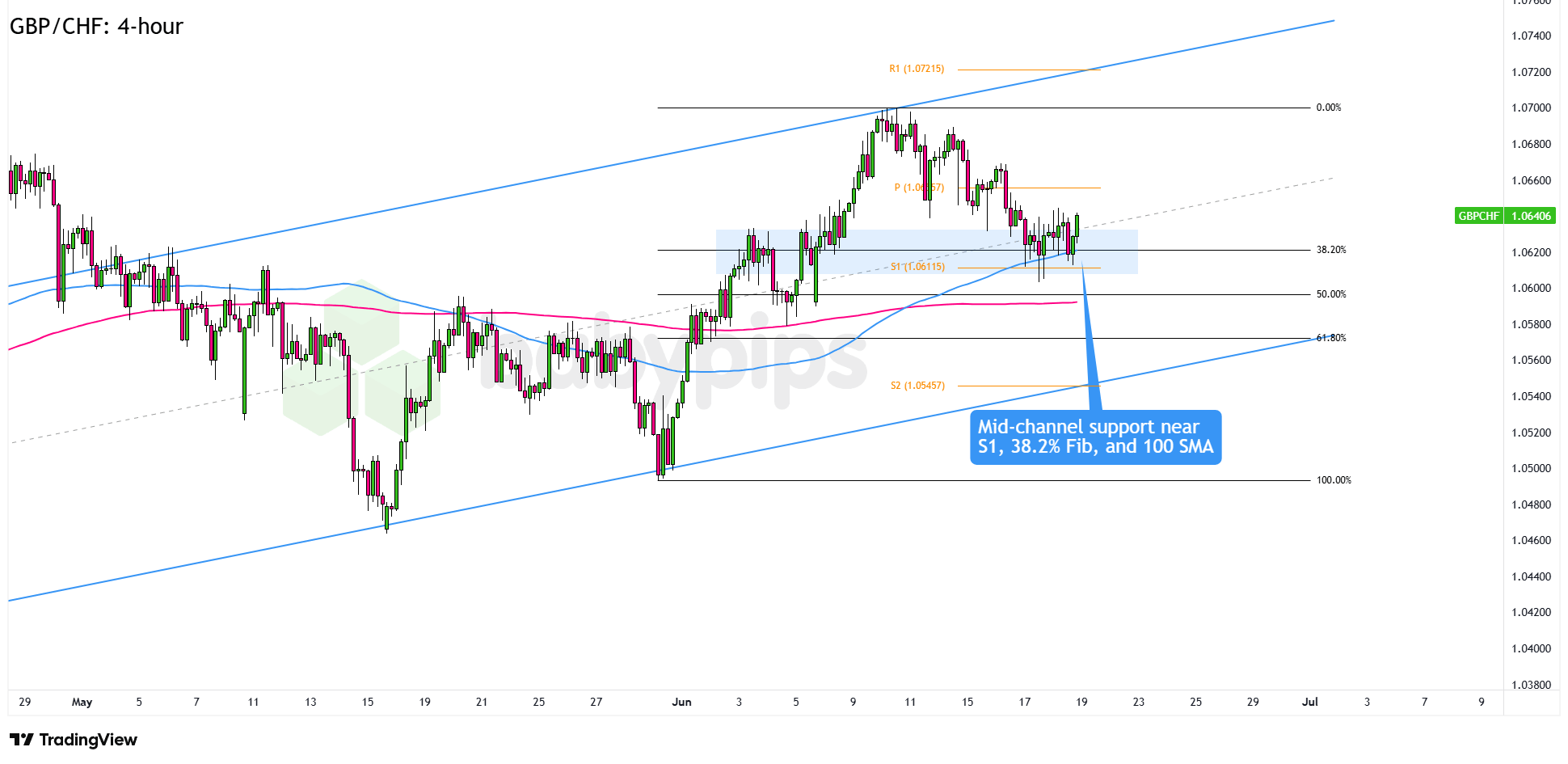

Market Shocks Ahead: Uncover the Surprising Twists in the April 23, 2026 Financial & Forex Landscape

Ever wonder how a single geopolitical spark can ripple through global markets like a stone skipping across a pond? Thursday’s trading session certainly answered that—escalating tensions in the US-Iran peace process sent WTI crude oil prices rocketing while stocks took a step back, unsure where to put their feet. The US dollar flexed its muscles, cruising to become the top-performing major currency, fueled by surprisingly strong US flash PMI data, while safe havens like gold and Bitcoin quietly retreated, nerves tingling amid the chaos. It’s a vivid reminder: in today’s markets, a headline isn’t just news—it’s a catalyst that can reshape fortunes in minutes. Curious about what else shook up the forex landscape? Dive into the latest on manufacturing beats, credit card spending surprises, and that eyebrow-raising order from President Trump about the Strait of Hormuz—it’s all here, and trust me, you don’t want to miss a beat. LEARN MORE.

Geopolitical tensions surrounding the stalled US-Iran peace process dominated Thursday’s trading session, as escalating rhetoric over the Strait of Hormuz drove WTI crude oil sharply higher while equities retreated from recent gains. The US dollar closed as the best-performing major currency on the day, likely supported in part by a stronger-than-expected slate of US flash PMI readings, while gold and Bitcoin both retreated as caution prevailed across risk assets.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Australia S&P Global Manufacturing PMI Flash for April 2026: 51.0 (49.0 forecast; 49.8 previous)

- Australia S&P Global Services PMI Flash for April 2026: 50.3 (46.0 forecast; 46.3 previous)

- Japan S&P Global Manufacturing PMI Flash for April 2026: 54.9 (50.1 forecast; 51.6 previous)

- Japan S&P Global Services PMI Flash for April 2026: 51.2 (52.0 forecast; 53.4 previous)

- New Zealand Credit Card Spending for March 2026: 2.1% y/y (29.0% y/y forecast; -1.1% y/y previous)

- U.K. Public Sector Net Borrowing Ex Banks for March 2026: -12.6B (-15.0B forecast; -14.3B previous)

- France Business Confidence for April 2026: 100.0 (98.0 forecast; 99.0 previous)

- Euro area S&P Global Manufacturing PMI Flash for April 2026: 52.2 (51.0 forecast; 51.6 previous)

- Euro area S&P Global Services PMI Flash for April 2026: 47.4 (49.7 forecast; 50.2 previous)

- U.K. S&P Global Manufacturing PMI Flash for April 2026: 53.6 (49.7 forecast; 51.0 previous)

- U.K. S&P Global Services PMI Flash for April 2026: 52.0 (50.0 forecast; 50.5 previous)

- Canada PPI for March 2026: 7.8% y/y (6.5% y/y forecast; 5.4% y/y previous); 2.4% m/m (1.3% m/m forecast; 0.4% m/m previous)

- Canada Manufacturing Sales Prel for March 2026: 3.5% m/m (2.2% m/m forecast; 3.6% m/m previous)

- U.S. Initial Jobless Claims for April 18, 2026: 214.0k (218.0k forecast; 207.0k previous)

- U.S. Chicago Fed National Activity Index for March 2026: -0.2 (0.2 forecast; -0.11 previous)

- U.K. Gfk Consumer Confidence for April 2026: -25.0 (-23.0 forecast; -21.0 previous)

- U.S. S&P Global Manufacturing PMI Flash for April 2026: 54.0 (52.0 forecast; 52.3 previous)

- U.S. S&P Global Services PMI Flash for April 2026: 51.3 (49.6 forecast; 49.8 previous)

- President Trump orders US Navy to shoot any boat placing mines in the Strait of Hormuz; US military confirms interception of two oil supertankers attempting to evade the blockade

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

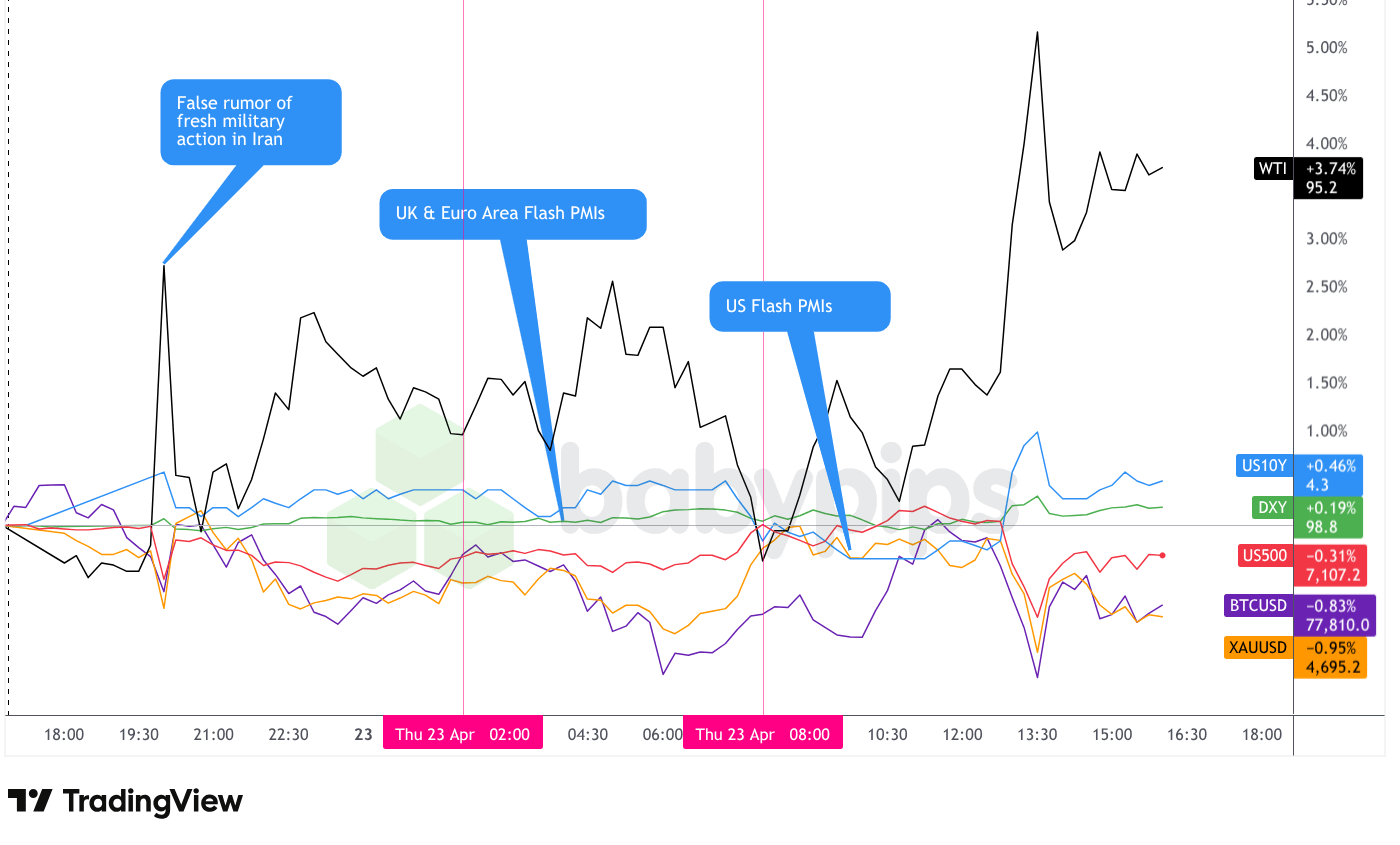

Broad Market Price Action:

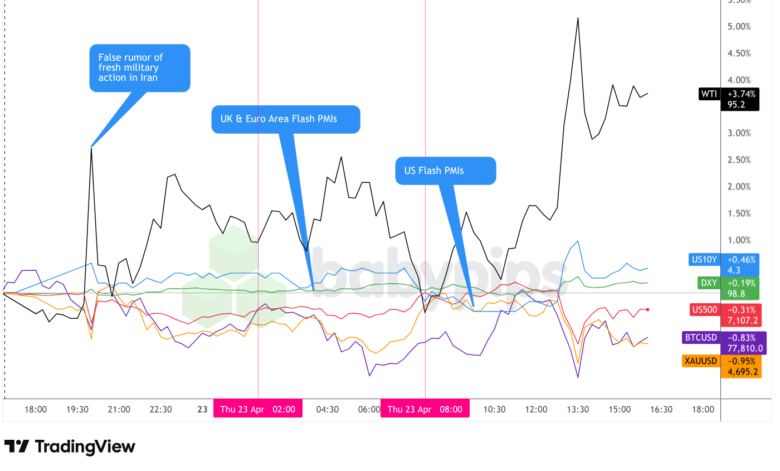

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Thursday’s session was defined by two overlapping forces: a fresh wave of Iran-related geopolitical anxiety and a robust batch of US economic data. The day opened with a false rumor of fresh military action in Iran circulating on social media, briefly rattling energy prices and equities during Asian trading before the reports failed to gain any official confirmation and the market reaction faded. Attention then shifted to a heavy data calendar, with UK and European flash PMIs landing during the London session and the US flash PMIs and jobless claims arriving ahead of the Wall Street open.

WTI crude oil was the session’s standout performer, rallying 3.74% to settle around $95.20 per barrel. The bulk of the advance appeared to correlate with a sharp escalation in US-Iran headlines around midday US time, as reports emerged that President Trump ordered the US Navy to shoot any vessel attempting to place mines in the Strait of Hormuz, and that US forces had intercepted two oil supertankers evading the blockade. Iran’s semi-official news agencies also reported air defense activations in parts of Tehran. With no clear plan to reopen the Strait of Hormuz, the premium for supply disruption risk remained firmly in place, with Brent crude approaching $105 per barrel, according to Bloomberg.

The S&P 500 declined 0.32% to close near 7,106.8, paring sharper intraday losses that at one point had the index down as much as 1.3%, with lows briefly touching the 7,046 area. The index had pushed toward session highs near 7,147 ahead of the US PMI release, but the escalation in Iran-related headlines around 13:30 ET proved enough to knock equity sentiment off balance. On the corporate side, Tesla fell after its latest earnings showed plans for increased capital expenditure that overshadowed better-than-expected profit results. IBM and ServiceNow shares also declined following quarterly results that failed to ease investor concerns about the costs of artificial intelligence disruption. Texas Instruments was a notable exception, with its solid outlook lifting chipmakers for a seventeenth consecutive session. Meta Platforms and Microsoft also drew attention after both companies announced workforce reductions in an effort to offset AI-related spending. Despite Thursday’s pullback, the S&P 500 remains on pace for its best monthly performance since 2023, with nearly 80% of reporting companies beating first-quarter earnings estimates.

Gold declined 0.91% to close around $4,696.1. The precious metal held relatively well into early US trading but sold off sharply around 13:30 ET, coinciding with the surge in oil and the spike in bond yields. The move may have reflected dollar strength weighing on the dollar-denominated metal, along with possible profit-taking following gold’s recent record-setting run, though direct catalysts for the magnitude of the decline are difficult to pinpoint with certainty.

The US 10-year Treasury yield rose approximately 3 basis points to close around 4.318%, climbing alongside the oil price spike during the US session. The move possibly reflected a pickup in inflation expectations tied to the energy supply disruption, though the competing pull of risk-off positioning makes the directional read on yields somewhat ambiguous in this environment.

Bitcoin declined 0.69% to trade near $77,920, drifting lower alongside other risk assets. The cryptocurrency briefly pushed toward $78,724 during early US trading before the afternoon geopolitical escalation and equity sell-off contributed to the pullback.

Promoted: Pay Once. Trade Forever.

Most prop firms quietly drain your account with monthly subscription fees long before you ever see a payout. Tradeify operates differently — evaluations are a one-time purchase with no recurring charges. Pass the eval, get activated instantly, and keep more of what you earn. With ~$150M in verified payouts and growing, the math speaks for itself.

Learn More About Tradeify!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

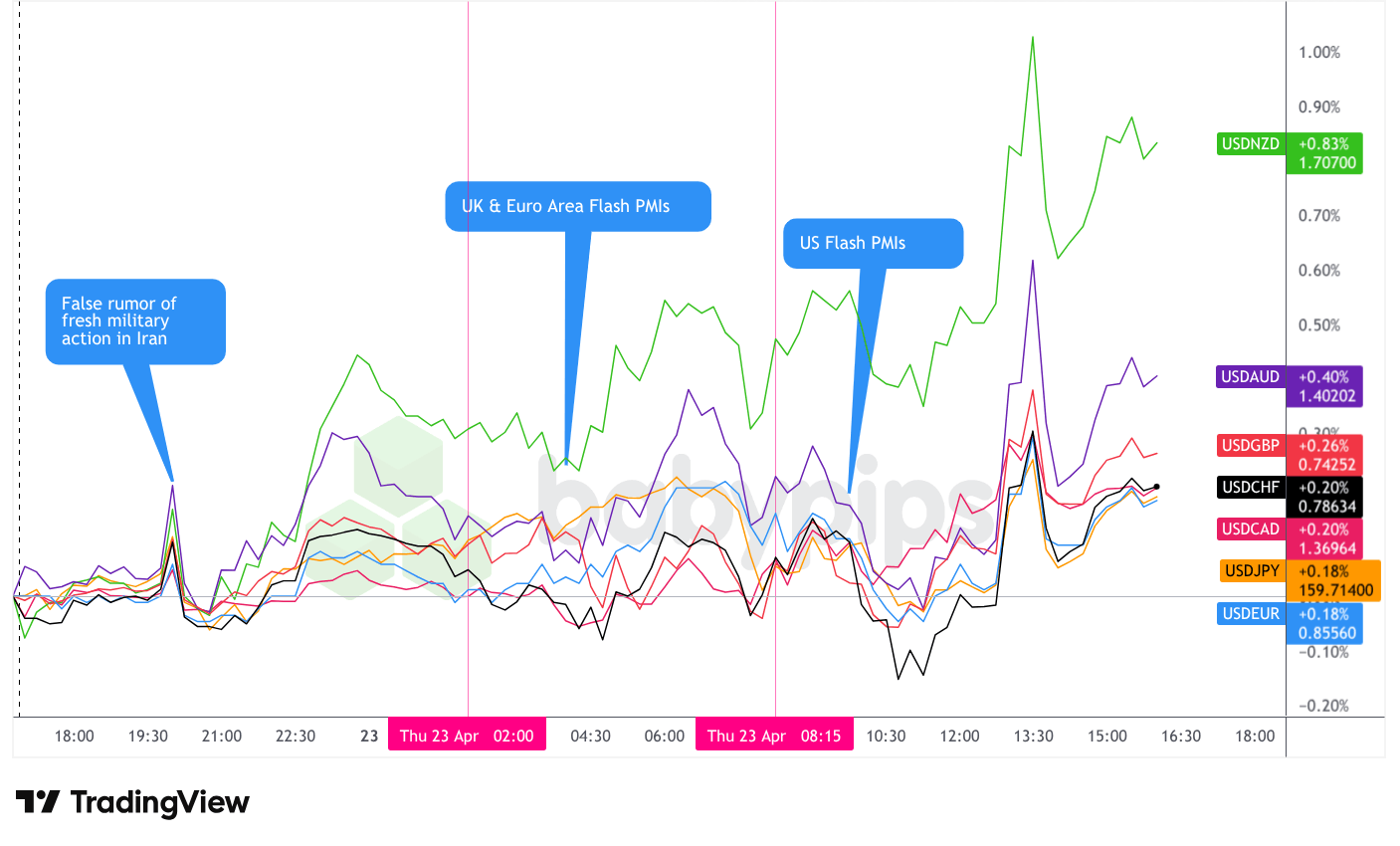

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The US dollar traded with relatively low overall volatility through much of Thursday’s session, though not without moments of sharp movement, ultimately closing as the best-performing major currency on the day against every major tracked here.

During the Asian session, the dollar moved mostly sideways with low volatility. The one notable exception was a brief spike in activity tied to social media rumors of fresh military action against Iran. The episode proved short-lived as the reports failed to gain official confirmation, and the dollar quickly settled back into a narrow range. Heading into the London open, the greenback carried a modest net bullish bias.

The London session continued the broadly sideways theme for the dollar, though volatility picked up as the European and UK flash PMI readings crossed the wires. The data offered a sharply mixed picture. The UK printed strong beats across both manufacturing (53.6 versus 49.7 forecast) and services (52.0 versus 50.0 forecast), while the eurozone painted a weaker picture, with services sliding to 47.4 against a 49.7 forecast and German services falling to 46.9 versus 50.5 expected. France’s services PMI also disappointed at 46.5. The manufacturing side of the eurozone was generally firmer, with France printing a notable beat at 52.8 against a 49.5 forecast and the broader euro area manufacturing PMI landing at 52.2 above the 51.0 estimate.

The UK CBI Business Optimism Index came in at a deeply negative -65.0, well below the -23.0 forecast, reflecting what industry representatives described as the most pessimistic view of business conditions since the Covid pandemic. Despite the mixed data backdrop, the dollar maintained a slight bullish bias through the London session without achieving any decisive directional breakout.

The US session brought heightened volatility for the dollar, with multiple dips and rebounds through the afternoon. The US flash PMI beats on both manufacturing (54.0) and services (51.3) and below-forecast jobless claims provided a supportive fundamental backdrop for the greenback. The intraday path was nonetheless choppy, likely reflecting the crosscurrents of the geopolitical escalation in oil markets, shifting equity-driven risk appetite, and repositioning flows around the economic data. The dollar finished the US session with a net bearish lean for that specific period, though the bullish carryover from the Asian and London sessions contributed to the greenback’s overall daily outperformance.

Upcoming Potential Catalysts on the Economic Calendar

- Japan Inflation Updates for March 2026 at 11:30 pm GMT

- U.K. Retail Sales for March 2026 at 6:00 am GMT

- France Consumer Confidence for April 2026 at 6:45 am GMT

- Germany Ifo Business Climate for April 2026 at 8:00 am GMT

- Canada Retail Sales Final for February 2026 at 12:30 pm GMT

- Canada Wholesale Sales Prel for March 2026 at 12:30 pm GMT

-

UoM U.S. Consumer Sentiment Index for April 2026 at 2:00 pm GMT

- Inflation & Consumer Expectations Final for April 2026 at 2:00 pm GMT

- Canada Budget Balance for February 2026 at 3:00 pm GMT

Friday’s calendar opens with Japan’s March inflation update late Thursday evening GMT, which will be watched closely against the backdrop of persistent yen weakness and the Finance Ministry’s repeated intervention warnings.

During the European session, Germany’s Ifo Business Climate reading will be in focus following Thursday’s sharply weaker German services PMI, offering the next gauge of corporate sentiment in Europe’s largest economy.

In the US session, the University of Michigan’s final April consumer sentiment and inflation expectations readings may attract particular attention given the elevated energy costs stemming from the Strait of Hormuz disruption. Any upward revision to inflation expectations could carry implications for the dollar and bond yields ahead of the weekend. The US-Iran diplomatic standoff remains the dominant macro narrative, and any weekend developments in the peace process or along the Strait could set the tone for Monday’s open.

Stay frosty out there, forex friends!

Promotion: When the Market Swings, Are You Reacting or Executing?

In “Positive Trading Psychology,” renowned psychologist Brett Steenbarger reveals in his newest book that the secret to navigating volatility like we’ve been seeing isn’t to “fix” your flaws—it’s doubling down on your innate character strengths. Learn how to stay clinical while the rest of the market is emotional, turning Wednesday’s geopolitical uncertainty into your professional edge.

Learn more about “Positive Trading Psychology: Turning personal strengths into trading strengths” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.