China’s CPI Surges to 3-Year Peak in December 2025—Is Deflation Still Lurking in the Shadows?

So, here’s a curious twist in China’s economic saga: consumer prices sprinted to their fastest pace in nearly three years last December, clocking in a 0.8% year-on-year rise — just a hair ahead of expectations. Meanwhile, on the factory floor, producer prices continue their marathon of deflation, extending an unbroken 40-month slide. Talk about a tale of two inflations! It begs the question — is this a sign of genuine consumer demand picking up steam, or just a seasonal mirage with base effects playing tricks? With factories still grappling with excess capacity and stubborn pricing woes, the economy’s balancing act teeters between hopeful acceleration and persistent headwinds. Could these mixed signals push policymakers to unleash more stimulus to keep the momentum going? If you’re intrigued by how these inflation dynamics might ripple across markets — especially given the muted but telling moves in the Aussie dollar — then you’ll want to dig deeper. LEARN MORE.

China’s consumer prices accelerated to their fastest pace in nearly three years in December while producer prices remained mired in deflation for a 40th consecutive month, reinforcing expectations for additional policy support.

Headline CPI rose 0.8% year-on-year versus the previous 0.7% gain as expected while the PPI slipped 1.9% year-on-year, better than the expected 2.0% decline and the earlier 2.2% slump.

Key Points

- CPI rose 0.8% year-on-year in December, the strongest increase since February 2023

- Monthly CPI climbed 0.2%, beating forecasts of 0.1%

- PPI fell 1.9% year-on-year, easing from November’s 2.2% decline but extending the deflationary streak beyond three years

- Core inflation held steady at 1.2% annually, suggesting underlying price pressures remain modest

- Food prices rose 1.1% year-on-year, while non-food prices increased 0.8%

The December inflation data presents a nuanced picture of China’s economic health. While the acceleration in consumer prices to 0.8% year-on-year marks the fastest pace since early 2023, the improvement appears largely driven by base effects and seasonal factors rather than robust underlying demand.

Link to official National Bureau of Statistics Chinese CPI and PPI (December 2025)

The persistence of producer price deflation, now extending beyond three years, signals ongoing challenges in China’s industrial sector. Excess manufacturing capacity and weak pricing power continue to plague factories, underscoring subdued business-to-business demand and competitive pressures that are forcing companies to absorb costs rather than pass them through.

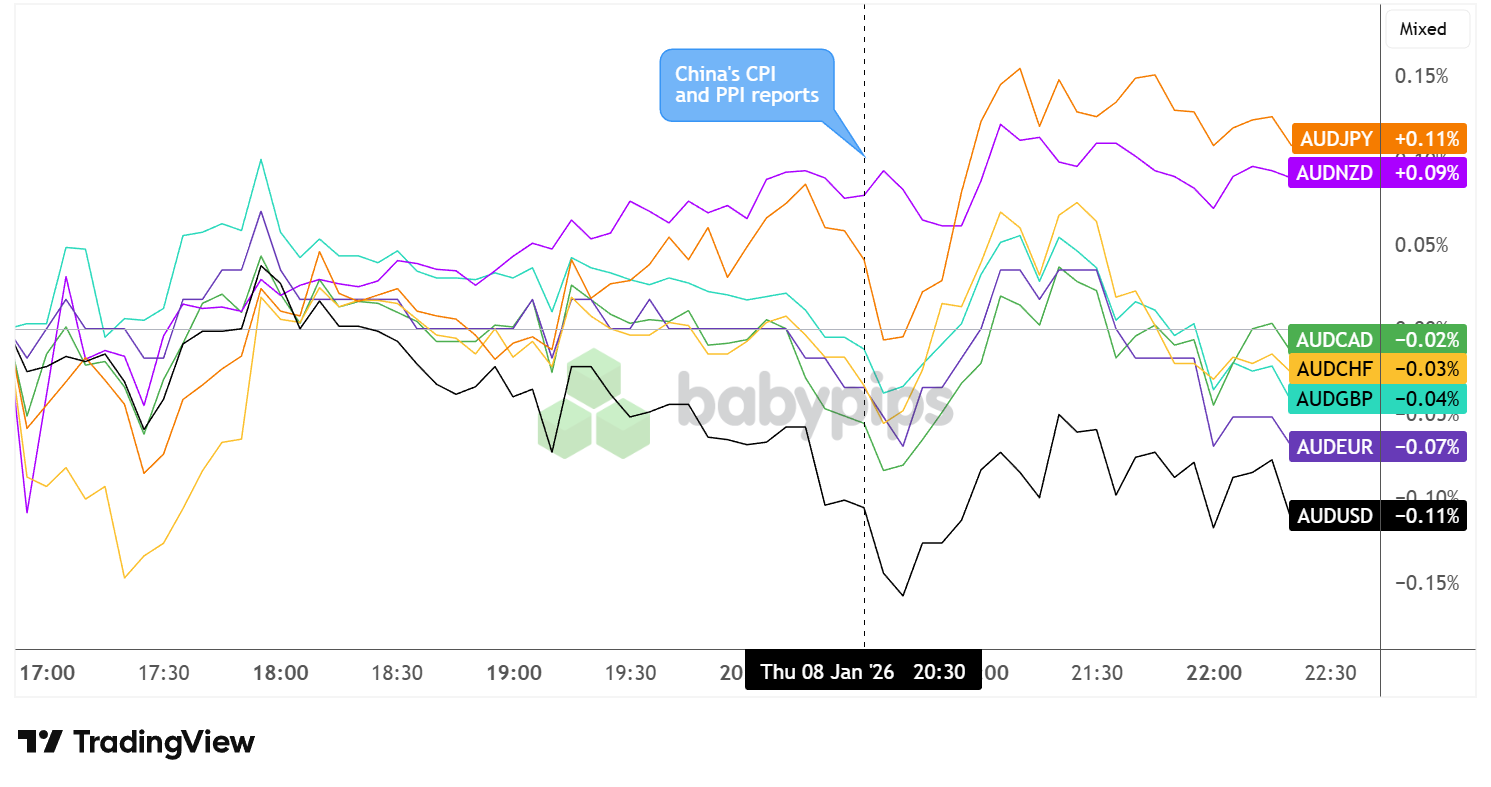

Market Reaction

Australian Dollar vs. Major Currencies: 5-min

Overlay of AUD vs. Major Currencies Chart by TradingView

The Australian dollar showed limited immediate reaction to the Chinese inflation data, with currency movements appearing relatively muted across major pairs in the immediate aftermath of the release.

The results triggered an initial dip, particularly against USD (-0.11%) and EUR (-0.07%), but the currency quickly found a bottom and turned higher within minutes after the report.

The Aussie even recovered above pre-CPI levels against NZD (+0.09%) and JPY (+0.11%) roughly an hour afterwards, suggesting that the possibility of additional Chinese stimulus could prove bullish for the currency.

The subdued market response likely reflects the mixed nature of the report: while headline inflation improved, the persistent producer deflation and modest core readings suggest China’s demand environment remains challenging.