Why Africa’s Payment Friction Could Be Its Greatest Financial Advantage—And What It Means for the Future

Ever wonder why the flawless, frictionless ecommerce checkout—the one where you pop in your address, punch your card details, and smugly wait for that sweet delivery—seems almost too good to be true in many parts of Africa? Well, buckle up. Over there, handing over your digital payment info isn’t just clicking a button; it’s a leap of faith wrapped in a healthy dose of skepticism. Consumers hit “Buy,” sure, but before they even think about payment, they want to see receipts—literally. Real-time photos on WhatsApp, delivery timelines, voice notes to prove there’s a human behind the screen—it’s like customer verification on steroids. This isn’t just cautious shopping; it’s a whole different ballgame shaped by trust, memory, and local realities. So, if you think your slick online checkout is the golden ticket, think again—because here, connection trumps convenience every time. LEARN MORE.

The ideal ecommerce checkout is frictionless and linear: enter one’s address and payment details and then await product delivery.

In Africa, providing digital payment info is a leap of faith. The checkout process is often conversational and skeptical.

Consumers may click “Buy,” but they aren’t reaching for their payment details. They first need proof of the product and company. They may ask via WhatsApp for real-time product photos and delivery timelines. They might demand a voice note to ensure a human is on the other side of the screen. It’s a do-it-yourself verification system.

“Cautious consumers” is McKinsey & Company’s term for Africa and Middle East-based ecommerce shoppers in its 2020 report (PDF).

Conversational Commerce

It is a mistake to view this reliance on WhatsApp as a workaround. For consumers in Africa, a WhatsApp chat is akin to looking a seller in the eye.

Consider the January 2026 partnership in Nigeria between PayPal and Paga, the mobile payment platform. After two decades of restrictions, Nigerians could finally receive international funds from PayPal into their Paga wallets.

The reception, however, was not great. Freelancers flooded Nigerian X with vitriol and skepticism stemming from a long memory of frozen PayPal funds.

This collective memory creates a psychological barrier that the partnership may struggle to overcome.

Trust

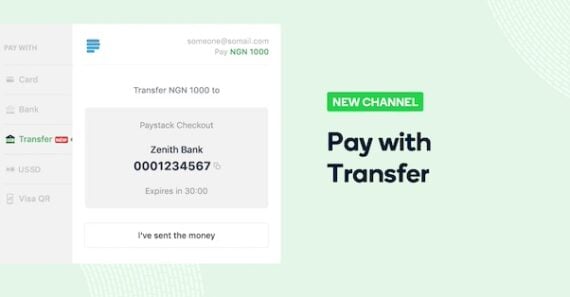

Paystack’s instant bank transfer settles transactions in one day.

Local payment platforms such as Flutterwave and Stripe-owned Paystack have succeeded because they understood consumers’ memories of money restrictions and failed transactions. The infrastructure of both reflects how people actually move capital.

Bank transfers. In Nigeria, merchants need settlement within one day of the transaction to keep their businesses running. For the customer, the transfer is final and verifiable.

M-Pesa. In Kenya, STK Push is a consumer-controlled security protocol enabling money transfers on mobile devices. Africa accounts for roughly 70% of global mobile money payments; ignoring STK Push is costly.

Kiosks. In Egypt, consumers often demand physical confirmation before payment. Fawry’s cash-at-kiosk model allows shoppers to order online but pay at one of thousands of physical kiosks.

Success

Foreign ecommerce merchants cannot buy their way into Africa with tech alone. Success comes from leaning into the friction consumers require.

- Use social media to consummate transactions. In Africa, an abandoned cart could mean that a shopper is waiting for the merchant on WhatsApp to prove it’s real.

- Localize the rails. Don’t force a Kenyan to use a Visa card or a Nigerian to rely on an international gateway that might flag the transaction as high risk. Use recognizable payment methods such as instant transfers, mobile payments, and in-person dialogue.

- Invest in the boring stuff. Don’t invest excessively in technology while ignoring operations. Logistics and customer support are where trust is either cemented or broken.