U.S. Core Inflation Holds Steady at 2.8% in November—Is the Fed’s Next Move Already Written?

So, here’s the curious case of the U.S. core Personal Consumption Expenditures (PCE) price index rising 2.8% year-over-year in November — just as the experts predicted, nudging up a tad from 2.7% in October. Now, you might be wondering, “Why does a tenth of a percent make news?” Well, those decimal points are like the secret sauce spicing up inflation’s story, signaling that price pressures are still hanging stubbornly above the Fed’s 2% comfort zone. Despite a gnarly 43-day government shutdown messing with data collection — forcing the Bureau of Economic Analysis to plug gaps creatively — consumer spending kept chugging along, showing some grit. But don’t pop the champagne just yet; folks are dipping into savings, which have hit their lowest since 2022. Oh, and the dollar? It danced briefly on these numbers, then mellowed out as geopolitical drama took center stage. Intrigued yet? Let’s unpack what’s really going on beneath these numbers. LEARN MORE.

The U.S. core Personal Consumption Expenditures (PCE) price index rose 2.8% year-over-year in November, matching expectations and ticking up from October’s 2.7% reading, according to data released Thursday by the Bureau of Economic Analysis (BEA).

The headline PCE price index also increased 2.8% annually, up from 2.7% in October and in line with forecasts. On a monthly basis, both headline and core PCE rose 0.2%, matching expectations.

Key Takeaways

- Core PCE rose 2.8% year-over-year in November, up from 2.7% in October

- Headline PCE also increased 2.8% annually, matching the core rate

- October and November data were released together due to the 43-day government shutdown

- Personal spending remained robust, rising 0.5% in both October and November

- Personal income growth slowed to 0.1% in October, then recovered to 0.3% in November

- Savings rate fell to 3.5%, the lowest level since October 2022

Link to U.S. Personal Income and Outlays Report for October and November 2025

The combined report for October and November came with significant caveats. Due to data collection disruptions during the government shutdown, the Bureau of Economic Analysis was forced to impute missing October Consumer Price Index data by averaging September and November figures—a methodology that raises questions about the October readings’ reliability.

Despite these distortions, the underlying inflationary trend remains clear: price pressures continue to run above the Federal Reserve’s 2% target. Consumer spending showed surprising resilience, with real personal consumption expenditures rising 0.3% in both months, driven by increased outlays on health care, gasoline, motor vehicles, and financial services.

However, this spending strength came at a cost. The personal saving rate dropped to 3.5% in November, its lowest point in over three years, as Americans dipped into savings to maintain spending levels. Personal income growth remained tepid, with disposable income barely rising after adjusting for inflation.

Market Reactions

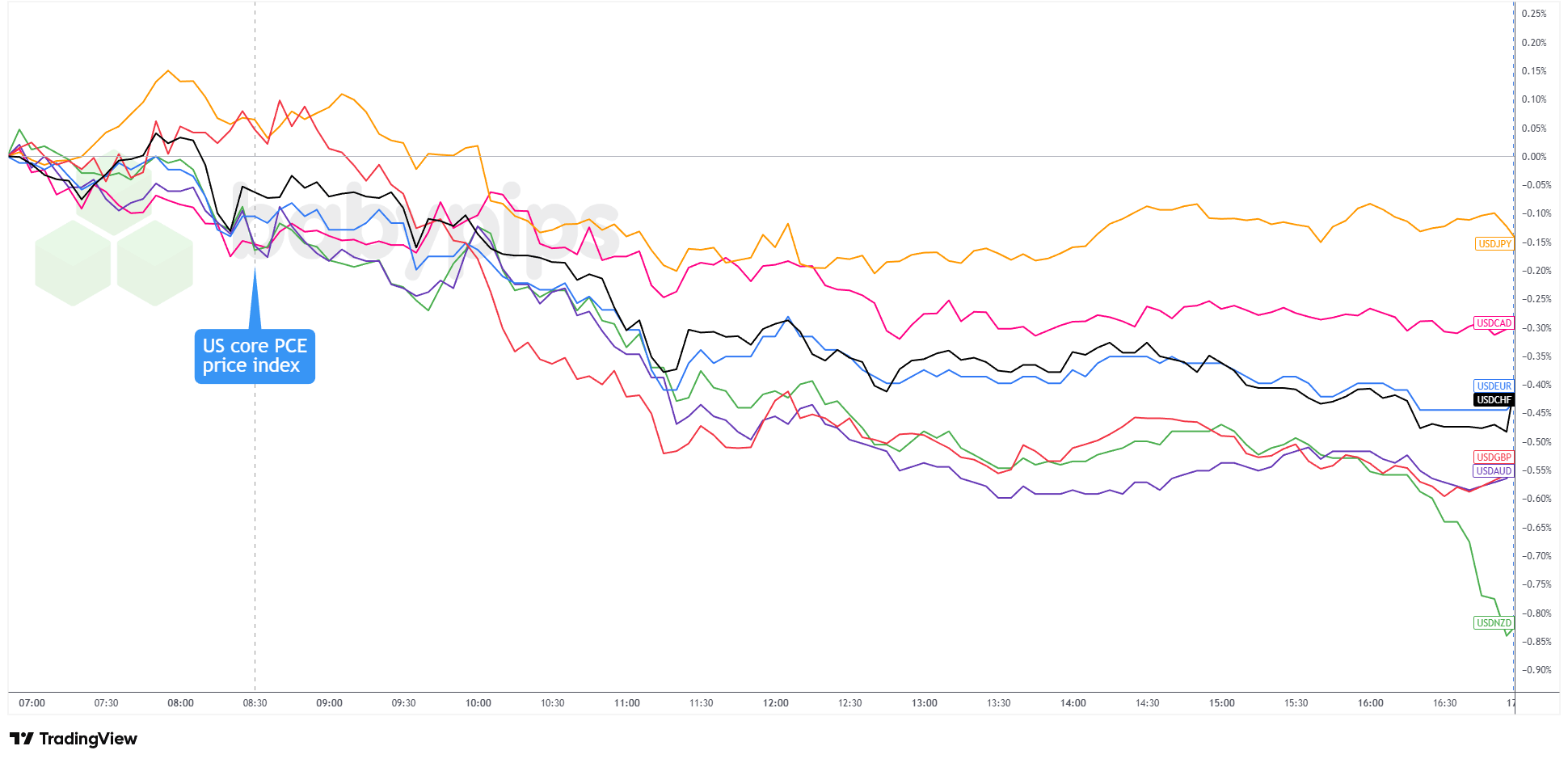

U.S. Dollar vs. Major Currencies: 5-min

USD vs. Major Currencies 5-min Forex Chart by TradingView

The U.S. dollar, which had been drifting lower ahead of the report, briefly bounced on the data release as the numbers appeared to back the Fed’s cautious stance on further easing.

However, the Greenback soon slipped back into a bearish tone as traders leaned into reduced safe-haven demand, easing geopolitical concerns following President Trump’s pullback on Greenland and NATO tariff threats, and likely some profit-taking after recent gains.

By the U.S. close, the dollar finished in the red against the major currencies except the relatively weaker Japanese yen.

The muted reaction highlighted competing forces in the market. While the inflation data technically supported the Fed’s hawkish pause narrative, broader themes quickly took over.

Confidence was also restrained by lingering concerns around data quality linked to the government shutdown, which likely discouraged traders from making aggressive directional calls. With Fed officials widely expected to leave rates unchanged at the late January meeting, the November PCE figures did little to shift the policy outlook.

Looking ahead, December’s PCE report due February 20 should offer a cleaner read on inflation trends without shutdown-related distortions. Until then, FX markets appear more focused on geopolitical headlines and swings in risk appetite than on economic data clouded by collection issues.