Is STRC Preferred Stock a Hidden Time Bomb? Analyst Warns of Massive ‘Dislocation’ Risk Ignored by Investors

Ever wonder what happens when investors start treating a financial instrument like it’s got an expiration date—when, in reality, it just goes on and on, like a sitcom that never ends? That’s exactly the conundrum Matt Dines, the savvy CIO over at Build Markets, points out about perpetual preferred stocks, especially Strategy’s Variable Rate Series A Perpetual Stretch Preferred Stock (STRC). These stocks don’t have a maturity date, meaning issuers can pay dividends forever without any pressure to pay back the principal. Sounds dreamy, right? But here’s the twist: if you’re holding these stocks and feel the urge to cash out, the only way is through the tricky secondary market—exposing you to endless liquidity and interest rate risks. As Dines warns, if market spreads widen, investors might be in for a wild ride that could shake things from the fiat side down. Meanwhile, STRC’s trading volume is hitting record highs as Strategy doubles down on using these perpetuals to fuel their Bitcoin stash. But just like any binge-worthy series, there’s a cap looming—$28 billion is the current issuance ceiling, and if it’s not raised, the BTC accumulation might hit a hard stop next year. The dividends, trading price, and variable yields add layers of intrigue to this ongoing saga. So, is STRC a clever play or a ticking time bomb disguised in steady payouts? Well, that’s the million-dollar—or should I say, million-Bitcoin—question. LEARN MORE.

Investors are mispricing risk for perpetual preferred stocks, like Bitcoin treasury company Strategy’s Variable Rate Series A Perpetual Stretch Preferred Stock (STRC), according to Matt Dines, the chief investment officer of credit asset management company Build Markets.

The corporate issuers of perpetual preferred stocks never have to repay holders their principal investment, and can just pay dividends indefinitely, without renegotiating the investment terms, Dines told the Truth for the Commoner (TFTC) media outlet.

If holders want to cash out, they must sell the perpetuals on the secondary market to recover their principal, which leaves holders exposed to liquidity contraction and interest rate risks that exist forever because perpetuals lack a maturity date, he said. He added:

“If spreads start to rise and the market demands higher yields from corporate borrowers, you also have to attach that to the infinite duration of the perpetual. So, if this dislocation comes in liquidity, it will come from the fiat side.”

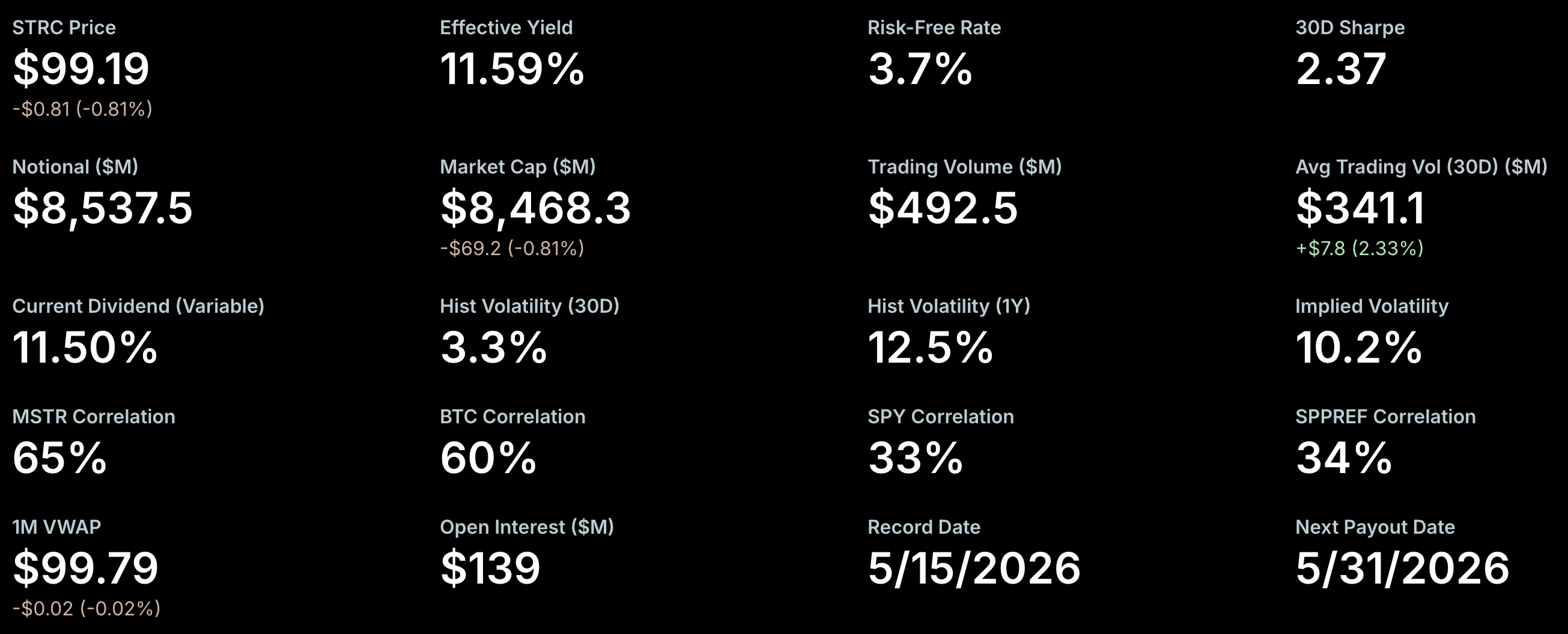

Basic performance metrics for Strategy’s STRC perpetual preferred stock. Source: SaylorTracker

The analysis comes amid growing demand for STRC; on Thursday, its daily trading volume surged to $1.5 billion, a new record for the financial instrument, as Strategy leans into preferred stock issuance to fund its Bitcoin purchases.

Related: Strategy to repurchase $1.5B of 2029 convertible notes

Strategy’s preferred funding vehicle may hit a ceiling in the next year

STRC currently has an authorized issuance cap of about $28 billion, according to crypto research company Delphi Digital.

If the authorized issuance cap is not raised before the $28 billion threshold, the company’s BTC accumulation may slow down, Delphi’s researchers said.

The total notional face value of outstanding STRC shares already sits at $8.5 billion, with the total market value of all outstanding shares at the time of this writing totaling about $8.4 billion.

STRC is trading at about $99 per share at the time of publication and carries a dividend rate of 11.5%, according to Strategy.

Detailed STRC performance metrics. Source: Strategy

The preferred stock’s dividend rate is variable, meaning that the yield offered to investors is subject to change on a monthly basis.

Strategy has also opened up voting for its common equity and STRC holders to approve semi-monthly dividend payments.

Magazine: Bitcoin’s ‘biggest bull catalyst’ would be Saylor’s liquidation: Santiment founder