Market Shocks Unveiled: What November 17, 2025, Reveals That Could Change Your Portfolio Forever

Ever get that feeling that the markets are playing some cosmic game of tug-of-war with your nerves? Monday was exactly that — investors caught between holding their breath for delayed U.S. economic data and trying not to flinch at mixed signals from the Fed. The S&P 500 slipped below a crucial technical line—after a long undefeated streak—just as AI valuations sparked fresh debates ahead of Nvidia’s much-anticipated earnings. And if you thought Bitcoin was safe after hitting sky-high records last October, think again — it kept sliding, erasing nearly all its 2025 gains. Meanwhile, the dollar quietly flexed its muscles amid the chaos, underscoring that in this market maze, resilience might be the name of the game. Curious how these puzzle pieces fit together and what’s next on the horizon? Dive into the latest twists and turns you may have missed. LEARN MORE.

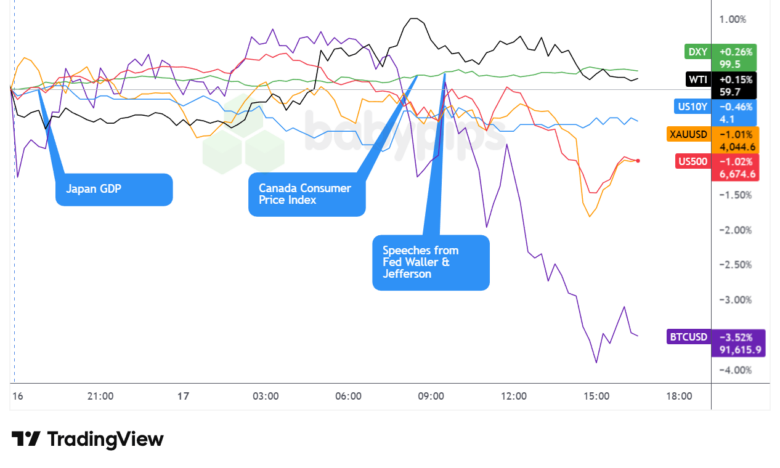

Markets entered a defensive stance on Monday as investors grappled with conflicting Fed signals, mounting concerns about AI valuations, and anticipation of delayed economic data releases following the U.S. government shutdown.

The S&P 500 declined 1.02% to close at 6,674.6, breaching its 50-day moving average after holding above that technical level for 138 consecutive sessions. The selloff was broad-based, with over 400 stocks in the index declining as technology shares faced pressure ahead of Nvidia’s Wednesday earnings report. The breach of this key technical threshold is likely driven by concerns about stretched AI valuations despite strong corporate fundamentals, and uncertainty with Fed rate cuts in December.

Gold retreated 1.01% to $4,044.6 per troy ounce as investors scaled back expectations for a December Fed rate cut. The precious metal pulled back from recent highs as Fed officials continued to offer mixed signals today on the path forward for monetary policy, with markets now pricing just 43% odds of a December cut compared to 62% a week earlier.

WTI crude oil edged up 0.15% to $59.70 per barrel, finding modest support despite ongoing concerns about global demand and potential OPEC+ production adjustments. Energy prices traded in a narrow range as traders awaited clearer direction from economic data.

Bitcoin suffered sharp losses, plunging 3.52% to $91,615.9 as the cryptocurrency extended its retreat from October’s peak above $126,000. The digital asset has now erased its 2025 gains, with the total market value declining approximately $600 billion from October highs. The selloff reflected waning risk appetite and diminished conviction despite institutional infrastructure and political support remaining in place.

The 10-year Treasury yield declined 0.46% to settle around 4.13%, retreating modestly as bond markets priced in ongoing uncertainty about the Fed’s December decision and absorbed mixed labor market signals from Fed officials.

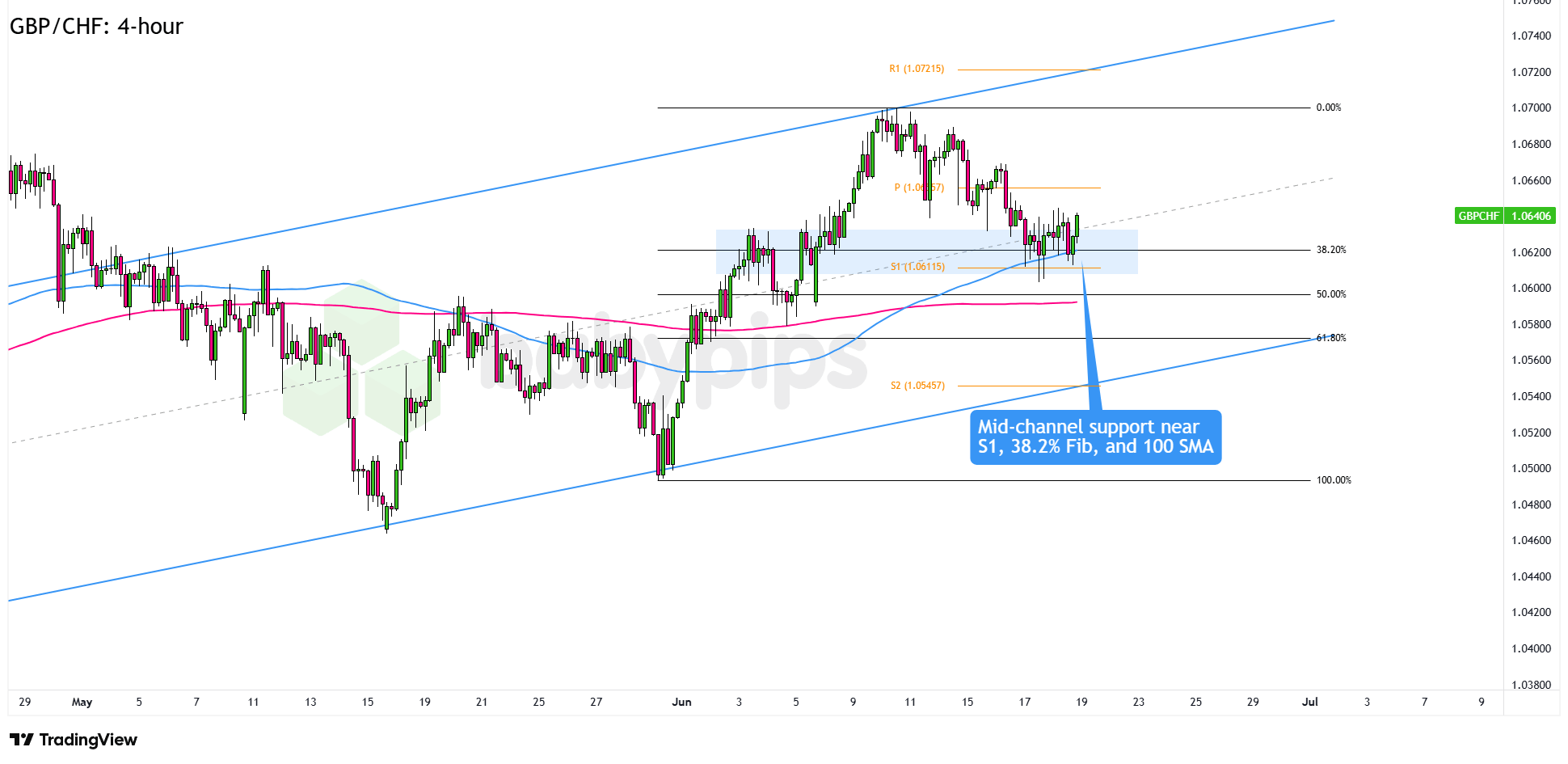

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Majors Forex Chart by TradingView

The U.S. dollar displayed resilience on Monday, closing as the session’s strongest major currency despite experiencing notable intraday volatility that reflected market uncertainty about Federal Reserve policy direction and delayed economic data releases.

During the Asian session, the greenback rallied initially before pulling back toward opening levels ahead of the London open. No notable U.S. catalysts, but the markets digested Japan’s Q3 GDP contraction and processed escalating tensions between China and Japan over Taiwan-related comments, which likely created mixed safe-haven flows across currencies, possibly benefitting USD on net.

The London session opened with the dollar dipping initially, but the weakness proved short-lived. The greenback quickly found support and rallied through the remainder of the morning European session as traders likely focusing on positioning ahead of the week’s key events with no notable catalysts to focus on.

During the U.S. session, the dollar maintained its net positive bias but traded largely sideways against major currencies. Federal Reserve Governor Waller’s speech advocating for a December rate cut to provide “insurance against labor market acceleration” initially weighed on the greenback, but the dollar recovered as Vice Chair Jefferson’s more cautious remarks about proceeding “slowly” with cuts balanced the dovish message. The conflicting Fed commentary left traders uncertain about the December meeting outcome, supporting defensive dollar positioning.

The dollar’s resilience despite mixed Fed signals and ahead of Thursday’s delayed September jobs report suggests markets are maintaining a cautious stance, with traders reluctant to establish aggressive positions until the backlog of U.S. economic data provides clearer direction on the labor market and Fed policy path.

Upcoming Potential Catalysts on the Economic Calendar

- Australia RBA Meeting Minutes at 12:30 am GMT

- U.S. Fed Logan Speech at 12:55 am GMT

- China FDI (YTD) YoY for October 2025

- Canada Housing Starts for October 2025 at 1:15 pm GMT

- U.S. ADP Employment Change Weekly for November 1, 2025 at 1:15 pm GMT

- U.S. NY Fed Services Activity Index for November 2025 at 1:30 pm GMT

- New Zealand Global Dairy Trade Price Index for November 18, 2025

- U.S. NAHB Housing Market Index for November 2025 at 3:00 pm GMT

- U.S. Fed Barr Speech at 3:30 pm GMT

- U.K. BoE Dhingra Speech at 4:00 pm GMT

- U.S. API Crude Oil Stock Change for November 14, 2025 at 9:30 pm GMT

Tuesday’s calendar lacks top-tier economic releases, but markets will remain focused on several key themes.

Central bank commentary continues with speeches from Fed officials Logan and Barr, along with Bank of England’s Dhingra, which could provide additional clarity on policy outlooks.

The U.S. ADP Employment Change Weekly report may offer preliminary signals about U.S. labor market conditions ahead of Thursday’s delayed September payrolls data.

Geopolitical tensions between China and Japan bear watching after Beijing’s escalation over Taiwan-related comments, with potential implications for regional trade and investment flows. Global tariff developments remain a wildcard, particularly regarding U.S.-EU steel and aluminum negotiations and ongoing reciprocal tariff discussions with various trading partners.

With most delayed U.S. economic data still lacking specific release dates, markets may continue trading in relatively muted ranges as investors await clearer catalysts later in the week.

Stay frosty out there, forex friends, and don’t forget to check out our Forex Correlation Calculator when planning to take on risk!

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView